Stock Forecast:

[Source: Wikimedia Commons]

“At Netflix, we think you have to build a sense of responsibility where people care about the enterprise. Hard work, like long hours at the office, doesn’t matter as much to us. We care about great work”

— Netflix CEO Reed Hastings

Netflix now has 125 million members worldwide

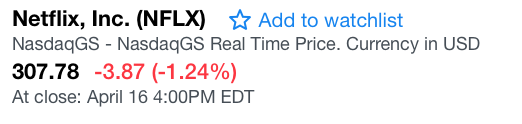

Shortly after Netflix (NFLX) published their Q1 Earnings Report after market hours on April 16th, 2018, Netflix’s stock soared from a closing price of $307.78 to $323.75 per share after hours, increasing roughly 7% before the market open alone. Over the past year, Netflix has outperformed the market by more than 102%. Upon examining the drivers behind this impressive growth that occurred within the past year, the most recent earnings report published by Netflix provides insight as to their stock event, as well as success over the past year.

Netflix stock soared on Tuesday after Netflix has added 7.41 million subscribers (1.96 million in the US, and 5.46 million outside the US), which had beat expectations for the first quarter. Netflix, as a highly successful streaming company, posted their quarterly earnings that crushed expectations and impressive revenues that reached above estimates. The 7.41 million increase in subscribers are up from 4.95 million a year earlier and well ahead of the 6.6 million analysts surveyed by FactSet forecasted. It now has 125 million members worldwide. Paying customers rose 25% year over year and made up about 95% of Netflix’s subscriber base (the remainder use the service’s free trial for new members and other offerings). Revenue increased 43%, to $3.7 billion during the quarter year-over-year. It was the fastest pace of growth in the company’s streaming history, primarily due to a 25% increase in the av era paid streaming memberships and a 14% rise in ASP. Operating margin of 12% rose 232 bps year over year, and earnings were also up 60%. The subscriber user growth sets Netflix up for a bright outlook in the second quarter, as the company’s earnings guidance came in well above Wall Street’s forecast. Shares has risen 5% after hours as a result of the impressive metrics.

[Source: Quartz Media via Factset]

How did Netflix do in Q1?

- Earnings per Share (EPS): 64 cents adjusted vs. 64 cents expected by a Thomson Reuter’s consensus estimate

- Revenue: $3.7 billion vs. $3.69 billion expectations

- Total streaming nets adds: 7.41 million vs. 6.5 million expected.

- Domestic streaming net adds: 1.96 million vs. 1.48 million

- International streaming net adds: 5.46 million vs. 5.02 million

- Free cash flow was negative $287 million, compared with negative $524 million in Q4’17.

Netflix has relied on international growth and heavy investments in original content to drive subscriptions – and Monday’s results provided an update on their effectiveness. Netflix’s addition of more than 7.4 million international subscribers set a new record, marking growth of 50% from a year ago. Over the past year, Netflix has relied on international growth and heavy investments in original content to drive subscriptions, and Monday’s results provided an update on their effectiveness in this regard. Netflix’s addition of more than 7.4 million international subscribers set a new record, marking growth of 50% from one year ago. Over the past year, Netflix has shot original content in 17 countries as it focuses on more local programming as many of their foreign-language shows are considered successful hits on American cable channels, thanks to artful subtitling. CEO Reed Hastings added that Netflix has also seen success on its international mobile app offerings.

[Source: Quartz Media via Factset]

Additionally, Netflix also expects to have $7.5 billion to $8 billion of content expenses this year, which fell in line with previous estimates. They had also noted that they expect to grow to 60 million to 90 million members in the U.S. over time and that it would likely spend $8 billion on content and $2 billion on marketing this year. “We’re investing in more marketing of new original titles to create more density of viewing and conversation around each title,” the company said in a statement.

The company faces increase competition from Amazon and Disney, which have their own offerings, as well aa traditional media companies and technology firms such as Apple. Hastings said the company still has a long way to go to compete with the likes of YouTube, and noted that Netflix’s ability to raise prices depends on providing more value than competitors. During this time, and supplementing Netflix’s need to shine above competitors, Netflix recently launched bundle offers with Proximus (in Belgium), SFR Altice (France) and T-Mobile (US). They have proven to be very successful and they are now adding similar bundle offers with additional MVPD partners. Recently, Netflix announced that they are bundling the Netflix service with packages from Sky which will begin later this year and with Comcast in the US, which are currently being rolled out. These relationships allow these partners to attract more customers and to upsell existing subscribers to higher ARPU packages, while Netflix benefits from due to more reach, awareness and often less friction in the signup and payment process. Additionally, in March, they rolled out additional features providing members with greater information and control over their Netflix viewing.

Guidance for Q2:

- Forward guidance for Q2 EPS: 79 cents a share vs. 65 cents per share expected

- Forward guidance on Q2 revenue: $3.9 billion vs. $3.89 billion expected

- Forward guidance on net adds: 6.2 million global additions (1.2 m in the US and 5 for the international segment) vs. 5.24 million in Q1 ’17 (974,000 domestic and 4.27 million international)

- Q2 operating margin is expected to to be 12%, and a targeted operating margin of 10% – 11% for the full year

[Source: Factset via TheStreet]

Thus, based on the context above, it seems as Netflix’s impressive revenue increase and the fast paced environment that they belong in, will likely continue and serve them well in the coming months. The addition of new managerships, yet again, demonstrates their perseverance against competitors in the market, such as Apple, Disney and Amazon. Increased investments have also been helpful, as the firm wishes to create more density of viewing and conversation around each title. By partnering with a few select firms, Netflix is strategically placing themselves in a situation which allows for growth as the firm is investing assets into building more value for the firm in the near future.

As such, it can be noted that due to Netflix’s impressive subscriber growth due to their recent earnings report, Netflix’s stock increase of 102.04% fell in accordance with the algorithms predictions which had accurately predicted the said rise using artificial intelligence and machine learning prior to the earnings report published on Monday. Such an impressive stock hike outperformed the market by over 102% during the past year, and more than 5% over the past few hours alone as stocks climbed after hours.

[Source: Yahoo Finance, April 17th, 2018]

On April 5th, 2017. I Know First issued a bullish 1 Year forecast for NFLX stock. the forecast illustrated a signal of 144.15 and a predictability of 0.37. In accordance with the forecast, NFLX’s stock returned 102.04% over this annual period, highlighting the accuracy of the prediction produced by the I Know First algorithm. Below it can be seen that the stock path that the I Know First algorithm created, was in line with the stock market’s stock path, thereby showing the accuracy of the I Know First algorithm in predicting the direction of Netflix stock.

[Source: I Know First, April 17th, 2018]

Current I Know First subscribers received this bullish NFLX forecast on April 5th, 2017.

To subscribe today click here.

Netflix, Inc. (NASDAQ:NFLX), incorporated on August 29, 1997, is a provider an Internet television network. The Company operates through three segments: Domestic streaming, International streaming and Domestic DVD. The Domestic streaming segment includes services that streams content to its members in the United States. The International streaming segment includes services that streams content to its members outside the United States. The Domestic DVD segment includes services, such as digital optical disc (DVD)-by-mail. The Company’s members can watch original series, documentaries, feature films, as well as television shows and movies directly on their Internet-connected screen, televisions, computers and mobile devices. It offers its streaming services both domestically and internationally. In the United States, its members can receive DVDs delivered to their homes. The Company had members streaming in over 190 countries, as of December 31, 2016. Its subsidiaries include Netflix Entretenimento Brasil LTDA, Netflix K.K., Netflix International B.V., Netflix Streaming Services, Inc., NetflixCS, Inc. and Netflix Studios, LLC.

Disclaimer

Before making any trading decisions, consult the latest forecast as the algorithm updates predictions daily. You can use the algorithm for intra-day trading. The predictability tends to become stronger with forecasts over longer time-horizons such as the 1-month, 3-month and 1-year forecasts.

Please note-for trading decisions use the most recent forecast.

Get

Read More

This Netflix stock forecast article was written by Viktoriya Voronchuk – Financial Analyst intern

This Netflix stock forecast article was written by Viktoriya Voronchuk – Financial Analyst intern  Read The FullPremium Article

Read The FullPremium Article