NVDA Stock Forecast: Where is NVIDIA Stock Price headed?

Highlights

- NVIDIA achieved 58% gross margin and 21% net margin in the first 9 months of FY2023, its profitability positioning at the Top 20 Percent in the semiconductor industry.

- NVIDIA EPS will grow from $2.97 in the first 9-month level to $3.27 in the next period.

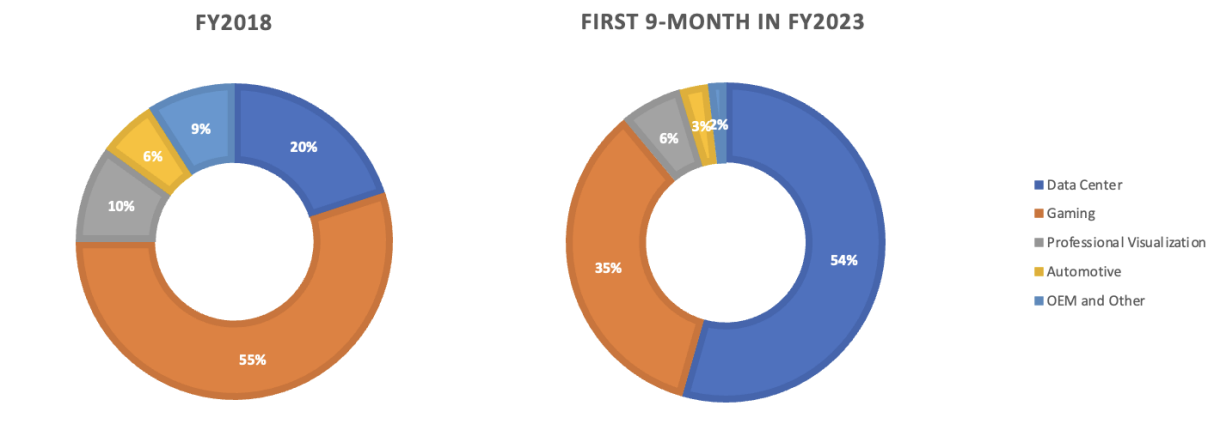

- Specialized segment Data Center and Automotive had positive growth in the first nine-month of 2022 while Gaming, Professional Visualization, and OEM and Other markets experienced downward due to an oversupply of products and lower demand expectations.

- DCF estimates NVDA stock will grow to $291, a 37% upside potential for the year 2023.

Overview

NVIDIA Corporation (NVDA) is a multinational technology company known for designing graphics processing units (GPUs), application programming interfaces (APIs), and system-on-a-chip units (SoCs). The firm depends on third parties to manufacture and assemble products as they don’t produce semiconductors. There are 5 specialized markets NVDA serves involving Data Centers, Gaming, Professional Visualization, Automotive, OEM and Other (Original Equipment manufacturers). NVDA was founded on April 5, 1993, by Jensen Huang (CEO as of 2022), Chris Malachowsky, and Curtis Priem and is headquartered in Santa Clara, California, U.S. The fiscal year 2023 is as of January 30, 2023.

Solid Performance and Promising Future

NVIDIA reorganized operating segments into two main parts in FY2021. One is Graphics and the other is Computer & Networking. In Q3 FY2023, the graphics segment earned $2.1 billion about 36% of the total revenue, with a 51.7% decrease from a year earlier. The computer and networking segment generated $3.8 billion about 64% of the total revenue, with a 26.7% increase compared to the last year. Revenue mainly comes from countries outside the U.S. accounting for 71% of the total (25% from Taiwan, 23% from China, and 23% from others) for the first 9 months of FY2023.

As a leader in the semiconductor industry, NVIDIA still performed well by achieving a gross margin of 58% in the first nine-month, 7% lower than the previous year. The negative impact is primarily due to $702 million in inventory charges, consisting of about $354 million for inventory on hand and $348 million for inventory purchase obligations beyond the demand forecasts.

Although the market experienced the worst GPU shortage from late 2020 and 2021, the current situation reveals retailers have overstocked GPUs and are facing troubles when clearing the inventories because of the lower market demand in a depressed economy. Therefore, the oversupply of GPUs hardly hit the NVDA Gaming segment’s profits but the negative impact is largely offset by the dramatic demand for the data center.

NVDA serves five specialized markets and the performance for each market in the first 9-month of FY 2023 showed as follows:

- Data Center earned 54% of the total revenue, increasing by 55% compared to the previous year. NVIDIA is the leader in AI training and inference and powers 361 of the TOP500 supercomputers. The biggest US cloud providers and a growing number of consumer internet companies were the main drivers of the steady rise. The development of autonomous driving, high-performance computing, and analytics in vertical industries like automotive and energy also fueled the growth. Simply put, the growth driver is the rapid AI adoption across industries.

- Gaming comprised 35% of total revenue, declining by 20% YoY, which reflects lower sell-in to partners due to lower demand expectations. After Q4 FY2023, the channel inventories are anticipated to return to their normal level. Although it did well in the Americas and Europe, sell-through was weaker in the Asia Pacific due to the difficult macroeconomic conditions. What’s more, NVIDIA believes the utility of GPUs for cryptocurrency mining has decreased as a result of the recent switch from proof-of-work to proof-of-stake for verifying Ethereum cryptocurrency transactions. This might have affected the demand for low-end devices.

- Professional Visualization accounted for 6% of total revenue, reducing by 10% YoY due to the gloomy outlook and lower market demand. But there are still long-term opportunities driven by ray tracing and AI revolutionizing design. As a leader in Workstation Graphics, NVDA has owned a 90%+ market share showing its strong ability for pricing.

- Automotive made up 3% of the total revenue, growing by 38% YoY, owing to the expansion of AI Automotive Solutions as the DRIVE Orin-based customers’ production ramps up. Dominated in Autonomous Driving, NVIDIA’s historical revenue is fueled largely by infotainment but its future growth will be primarily driven by the adoption of centralized car computing and software-defined vehicle architectures.

- OEM and Other took up 2% of the total revenue, dripping by 62% from a year ago. The decline was driven by lower Jetson and notebook OEM sales.

Two External Factors Affecting Business

Impact of US-China Trade Tensions

During the third quarter of FY2023, the U.S. government (USF) issued new license requirements that restrict exports to China (including Hong Kong) and Russia of A100 and H100 integrated circuits, DGX, or any other systems incorporated with certain circuits. These requirements also apply to any future NVIDIA integrated circuit having the same or better performance as A100, as well as the related system or board.

Apart from the restrictions, NVIDIA is also required to move certain operations out of China, which could be costly and time-consuming, resulting in a huge adverse impact on sales. Although the company has engaged with customers in China trying to satisfy their demand by providing alternative products and seeking a license, there are a lot of uncertainties that the alternatives might not meet up with expectations and USG might not grant licenses or act on them timely. These new restrictions have a disproportionate harm on NVIDIA but might benefit the competitors who are not subject to the new restrictions and have alternatives for our products and services. The negative impact on third-quarter revenue from these restrictions is not negligible but it’s largely offset by sales of alternative products in China up to now.

Business Closed in Russia

During the first quarter of FY2023, NVIDIA paused direct sales to Russia. This action was immaterial since Russia just accounted for about 2% of total end customer sales and 4% of Gaming end customer sales in FY2022. During the third quarter, the company closed its business operations in Russia.

Key Announcements in the Third Quarter

NVIDIA has declared the following announcements on new software and services.

Data Center

- The NVIDIA H100, a new addition to the NVIDIA AI Enterprise software suite, is currently in full production, and international tech partners anticipate releasing the first wave of goods and services in Q4.

- The NVIDIA NeMo LLM (Large Language Model) Service and the NVIDIA BioNeMo LLM Service, which are viewed as the most important two new AI models, have early access availability soon.

- The new Jetson Orin Nano system-on-module sets a new standard for entry-level edge AI and robotics, which was available in January 2023 starting at $199.

- Oracle Cloud Infrastructure (OCI) is adding tens of thousands more NVIDIA GPUs, including the A100 and upcoming H100, marking NVDA’s multi-year partnership with Oracle. A cloud-based AI supercomputer will be created via collaboration with Microsoft.

Gaming

- The Ada Lovelace GPU architecture enjoyed great popularity with tremendous demand and positive feedback. Specifically, GeForce RTX 4090 24GB is up to 4x faster compared to RTX 3090 Ti, which sold out quickly in many locations starting at $1,599. GeForce RTX 4080 16GB is 2x as fast as the RTX 3080 Ti and has more performance than RTX 3090 Ti at lower power, which was available in Q3 FY2023, starting at $1,199.

Professional Visualization

- NVIDIA OVX systems (Omniverse Computing Systems) are designed to build 3D virtual worlds and to operate immersive digital twin simulations in NVIDIA Omniverse Enterprise.

Automotive

- NVIDIA DRIVE Thor Superchip, with 2,000 teraflops of performance, has been selected by Geely-owned automaker ZEEKR for its next-generation intelligent EVs for early 2025 and the product will be available for automakers’ 2025 models.

Peers Comparison

Table 1: Comparison of NVDA’s Profitability in the first 9-month in the Semiconductor Industry

It’s obvious that NVIDIA has performed better than the industry median level and its profitability ratio almost all ranked about 80% better than the others. The strong profit earnings ability makes it attractive among investors and it’s no doubt that NVDA is the leader with a solid moat.

Table 2: Comparison of NVDA’s Valuation in the first 9-month in the Semiconductor Industry

NVDA had a higher valuation ratio compared to the industry median level, presenting the associated market expectations. Based on the historical analysis of its PE ratio, NVDA has always traded in a higher assessment compared to the others, which means investors are willing to pay more than what the stock is worth in relation to its earnings and are bullish on the NVDA stock forecast.

Positive Message Delivered from Stock Repurchase

Since NVIDIA’s offer to acquire ARM Holdings from SoftBank got shot down by regulators, the company used the idle cash and the current earnings to do stock repurchases to boost earnings per share by lowering the total shares outstanding. Through the first three-quarters of FY2023, NVIDIA has returned $8.83 billion to investors via share repurchases, including $3.49 billion in Q3.

This action can be deemed as a positive message for NVIDIA’s performance in the future from the managers’ perspective. Since the company operates in the cyclical depression periods and current sales went down compared to the previous year, its decision to buy back shares shows strong confidence in the full recovery of business operations and the increased demand for new products and services. With a reduced number of shares outstanding, it’s expected that NVDA’s EPS will grow from $2.97 in the first 9-month level to $3.27 in the next period.

Giant Market Opportunity

The worldwide IT spending is projected to total $4.5 trillion in 2023, an increase of 2.4% from 2022, according to Gartner, Inc. Among these, the software and IT services segment are forecasted to grow 9.3% and 5.5% in 2023 respectively, compared to 7.1% and 3.0% growth in 2022.

NVIDIA’s products and services can be deployed in industries such as gaming & metaverse, financial services, healthcare, logistics, manufacturing, retail, and transportation. It is expected to be a $1 trillion opportunity spreading among gaming ($100B), NVIDIA AI Enterprise Software ($150B), Omniverse Enterprise Software ($150B), Chips & Systems ($300B), Automotive ($300B).

DCF Values NVDA Stock at $291

The DCF analysis shows that NVDA’s intrinsic, 1-year, and 2-year stock price should be around $291, $321, and $351 respectively, which is 37%, 51%, and 65% upside potential from the price of $212.65 on Feb 12, 2023. It’s clear that the NVDA stock price is undervalued and is worth buying.

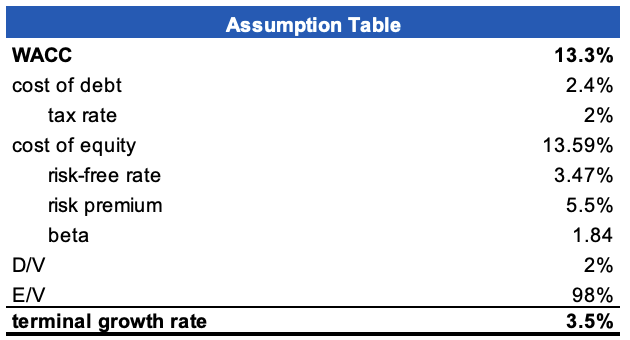

The DCF model is built based on the following assumptions:

- The risk-free rate is 3.47% according to the US 10-year zero coupon bond as of February 2023. The risk premium of 5.5% comes from the average market risk premium in the U.S. from Statista.

- Beta 1.84 is calculated based on the slope of the change of monthly NVDA stock price and S&P500 price from 2018 to 2023.

- The cost of debt is calculated as a weighted average interest expense of 2.4% and operating and finance lease discount rate of 2.7%, concluding at 2.4%.

- The tax rate is the effective tax rate of 2% derived from the 10-K by averaging the 2018 and 2022 figures.

- The terminal growth rate is assumed at 3.5%, which is the average GDP growth rate.

Due to the uncertainties in the macroeconomic environment, it is difficult to accurately predict the impact of relevant risk factors such as epidemics and wars, and the assumption may not be valid. A sensitivity matrix is created to show the impacts on NVDA stock forecast by altering WACC (weighted average cost of capital) and terminal growth rate.

Does Technical Analysis Support NVDA Stock Forecast for 2023?

NVDA’s 200-day moving average has still maintained an upward trend. The 15-day moving average line has turned up and is about cross the 50-day moving average. Besides, the MACD line has crossed the zero line and is above the signal line, showing a bullish momentum and signaling the price will continue to go up in the future.

A rectangle pattern was formed under the oscillating markets and there is an evident signal for the breakout. NVDA stock price is expected to grow to $267.51 in the recent period. The chart gives us a good sign that now is a good time to buy, confirming our fundamental analysis and DCF results for the NVDA stock forecast.

Viewpoints from Analysts Community

Based on Yahoo Finance, there were 38 analysts presenting recommendation trends for the NVDA stock forecast on February 2023, among which 21 recommended Buy, 15 Hold, and 2 Underperform. The recommendation rating is 2.2 between Buy and Hold. The average price target from 39 analysts is around $199.72 within the lowest $110 and the highest $329 price range.

From TIPRANKS, there are 22 Buys, 5 Holds, and 1 Sell from 28 analysts’ ratings in the last 3 months. The expected stock price is $209.19 within the lowest $136 and the highest $320 price range.

Conclusion

I take a buy-side on NVDA stock because the DCF target price is $291, a 37% upside difference from the current price. Although the FY2023 revenue growth rate is lower than the previous year due to the inventory charges and lower market demand, the company is strongly confident in its future development by launching new products and services and collaborating with the top companies. Its strong fundamentals support its stock repurchase, manifesting its positive expectations in the next periods.

It is worth paying attention that the stock-picking AI of I Know First has a high signal on the one-year market trend forecasts, supporting my position for the NVDA stock forecast. The light green for the short-term forecasts is mildly bullish, while the darker green is a strong bullish signal for the one-year forecast.

Past Success with NVDA Stock Forecast

I Know First has been bullish on the NVDA stock forecast in the past. On November 18th, 2022 the I Know First algorithm issued a forecast for NVDA stock price and recommended NVDA as one of the best computer stocks to buy. The AI-driven NVDA stock prediction was successful on a 3-month time horizon resulting in more than 36.43%.

To subscribe today click here.

Please note-for trading decisions use the most recent forecast.