V Stock Prediction: The Growing Digital Payments Industry Is Favorable To Visa

![]()

![]()

The article was written by Motek Moyen Research Seeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

V Stock Prediction

Summary:

- The king of credit cards, Visa is still flourishing during this new age of digital payments.

- As of 2016, Visa touts 335 million credit card customers in the U.S. Every digital payments leader like PayPal and Apple still has to pay tribute to Visa.

- Visa has 728 million credit cards in circulation worldwide. There are also 3.2 billion Visa-enabled payment/ATM/debit cards.

- Visa has recruited 13 new partners for its Token Service Provider (TSP). TSP is Visa’s secure payments solutions involving any smart device or Internet of Things appliances.

- Short and long term market trend algorithmic forecasts are still favorable to V.

Created originally in 1958, Visa, Inc. (V) still remains a global force during this new age of rising digital payments. In spite of PayPal (PYPL), Android Pay, and Apple (AAPL) Pay, I firmly believe that Visa will continue to prosper. Visa’s enormous influence in financial services makes it a necessary partner for any digital payments service provider.

Visa is still the king of credit cards. In the U.S. alone, there are 335 million Visa credit cards in circulation. Including other countries, there are 728 million Visa credit cards in circulation worldwide. Furthermore, the Visa Debit global program has also grown 3.2 billion of Visa-enabled payments cards.

(Source: Statista)

Visa Is Indispensable In Digital Payments Transactions

More often than not, digital payments leaders like PayPal, Apple Pay, and Android Pay still relies on a Visa credit or debit card to enable their services. Wary of attaching their main bank accounts to PayPal or Android Pay, a Visa credit/debit card is the go-to choice of many people who want to fund their digital wallets.

Visa, as the processor of payments and fund management gets a fee from every Apple Pay transaction. Without Visa’s platform, Apple Pay will be handicapped or inutile. All the in-app purchases and iTunes shopping done is achieved through a registered credit or debit card. Apple does not have its own global real-time payments processing system. Apple Pay, PayPal, and Android Pay are therefore mere gateways where Visa could make more money on people’s shopping activities.

(Source: Apple)

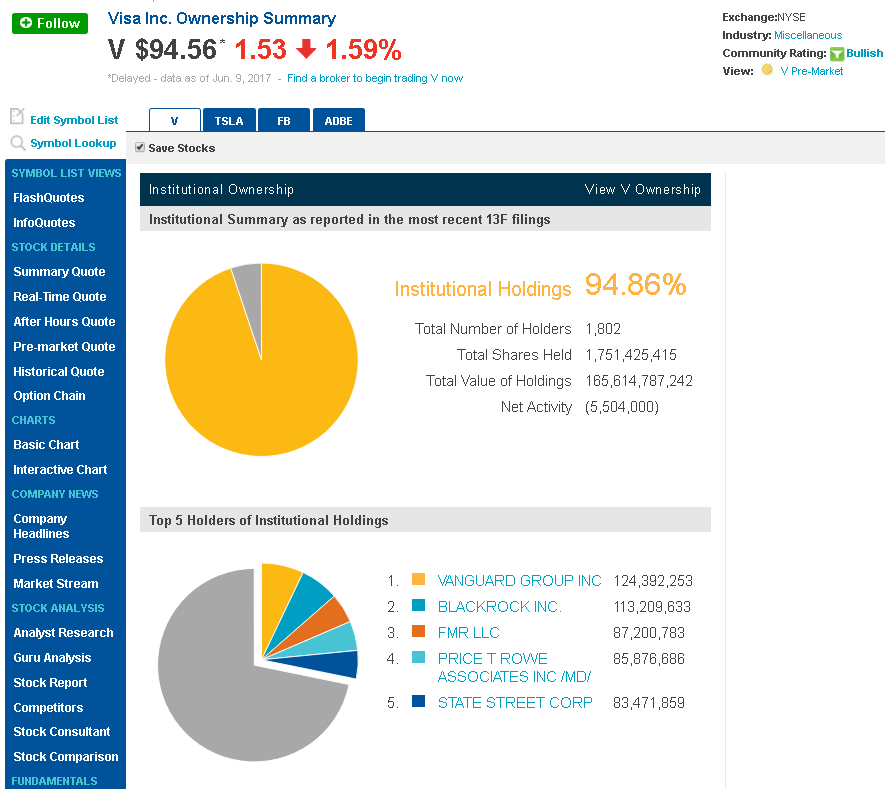

Visa’s unique Suez Canal-like control of digital payment transactions is why institutional investors own almost 95% of floated V shares. V is a long-term winner that is the biggest beneficiary of the rising digital payments industry.

(Source: Nasdaq.com)

In other words, the continuing success of PayPal, Apple Pay, and Android Pay depends a lot on the worldwide network first established by Visa’s credit/debit cards. Consequently, as more people get comfortable with online and mobile shopping, Visa credit card business will also prosper accordingly.

The impulsive-buying-habit-forming nature of mobile shopping is also beneficial to Visa. People will incur more credit card charges because of impulsive digital shopping. Consequently, Visa will get to charge more people (and more often) with 3% to 5% monthly interests on credit card charges. Credit card companies like it when people use their credit cards more often and with higher amounts of charges.

Visa’s generous loyalty points rewards system is also why it became such a global hit. I have a Gold Visa credit card and an American Express card. I never use the Amex card because the loyalty points reward system of Visa is far more rewarding. The measly 1% cash back rebate offer from Amex is worthless if you don’t charge with it at least $100,000 every year.

My point is that Visa knows how to reward loyal users of its credit cards. The more loyal users of Visa credit cards, the more attractive Visa is for e-commerce operators and digital wallet providers.

Final Thoughts

I rate V as a strong buy for long-term investors. Visa’s tireless innovation to improve its digital payments solutions is impressive. Visa’s VTS (Visa Token Service) has recruited 13 new partner Token Service Providers. Third-party Token Service Providers (TSPs) will help the global expansion of VTS. VTS is Visa’s new secured solutions to enable digital payments to and from any smart or Internet of Things-related devices and appliances. The Visa Token Service replaces cardholder information (credit card number, expiration dates, security PIN) with a unique digital identifier (or token).

Visa’s tokenization hides confidential information during wireless or digital transactions. VTS should make Visa even more attractive to PayPal, Apple Pay, and Android Pay. Visa’s long-term prosperity has always been due to its emphasis on finding new ways to secure payments.

My 10-year DCF Model: EBITDA Exit valuation for V is $110.85. That’s 17.2% upside potential for V.

(Source: Motek Moyen)

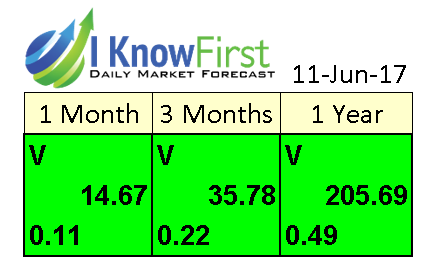

My bullish outlook for V is also supported by its positive algorithmic forecasts from I Know First. The 1-year market trend score of V is very high at 205.69. It means the stock has great probability of posting a higher price than what it has now, $94.56.

I Know First Algorithm Heatmap Explanation

The sign of the signal tells in which direction the asset price is expected to go (positive = to go up = Long, negative = to drop = Short position), the signal strength is related to the magnitude of the expected return and is used for ranking purposes of the investment opportunities.

Predictability is the actual fitness function being optimized every day, and can be simplified explained as the correlation based quality measure of the signal. This is a unique indicator of the I Know First algorithm. This allows users to separate and focus on the most predictable assets according to the algorithm. Ranging between -1 and 1, one should focus on predictability levels significantly above 0 in order to fill confident about/trust the signal.

Past I Know First Success With V

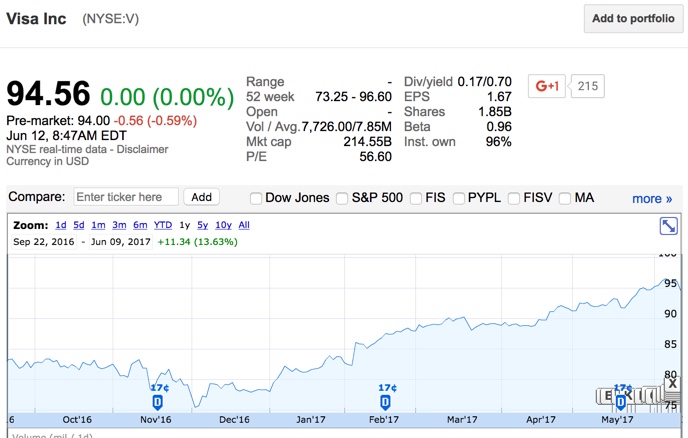

On September 22nd, 2016, I Know First’s very own Jacob Sapir wrote a Visa Stock Analysis. In the article he details Visa’s acquisition of Visa Europe to become one large global corporation. He also talks about the exclusive agreement with Costco as well as the switching to mobile in an effort to become digital and less plastic. Since the article was posted, Visa shares are up 13.63%.

An analysis of monthly technical indicators and moving averages agree with I Know First’s go-long recommendation for V.

(Source: Investing.com)

This bullish forecast for V was sent to I Know First subscribers on September 22nd, 2016. To subscribe today click here.