Apple Stock Analysis: Ignore The Bears And Buy Apple On The Pullback

![]()

![]() Naman Shukla is an Analyst at I Know First. He writes and invests in the stock market. Ranked in the top 8 percentile in TipRanks.com. Featured on SeekingAlpha.com, GuruFocus.com, Valuewalk.com among others.

Naman Shukla is an Analyst at I Know First. He writes and invests in the stock market. Ranked in the top 8 percentile in TipRanks.com. Featured on SeekingAlpha.com, GuruFocus.com, Valuewalk.com among others.

Apple Stock Analysis

Summary

- iPhone sales and Brexit concerns have pushed Apple’s stocks to unbelievably low levels.

- Apple’s success in India can offset some losses of U.S. market.

- Apple’s service segment is a massive tailwind.

- I Know First algorithm is currently bullish on Apple in long term

In the last three months, Apple’s shares (AAPL) have dropped approximately 15%. This weakness in the share price performance of Apple is due to a continued decline in the sales volumes of iPhone in the United States that accounted for nearly 65% of the company’s overall revenue in the last reported quarter.

Britain’s exit from the EU also caused some panic in the market, leading to a further decline in Apple’s shares that were already undervalued. Going forward, I think investors should make the most of this pullback and buy Apple while it is still trading at under $95.

Can iPhone SE help Apple to regain iPhone confidence?

The iPhone segment is one of the most critical businesses for Apple. However, the continued weakness in the iPhone sales has created a concern for investors. For instance, iPhone sales for the second quarter came in at $32.8 billion, a drop of approximately 18% as compared to the second quarter of 2015 and about a 36% decline on the sequential basis. This slump in the iPhone revenue is resulting from a steep turn down in the unit sales that decreased 16% to 51.2 million iPhone for the quarter, compared with a 61.2 million iPhone in the second quarter of 2015.

Source: Market Realist

The most concerning part is that Apple expects the iPhone sales for the third quarter of 2016 to decline to the tune of 15% to 19%, on the top of a 17% decrease in the iPhone sales in the second quarter of 2016. As a result of this decline, its overall revenue for the third quarter is forecasted to be in the range of $41 billion to $43 billion, way below consensus estimates of a $47.32 billion.

This weakness in the iPhone sales is due to a delay in the upgrade cycle as well as a decrease in the average selling price for iPhone. According to the management, the iPhone 6S had longer upgrade cycle slightly as compared to iPhone 6 that had a shorter upgrade cycle a year ago, leading to a 40% sales growth over the previous year. However, the company sees that upgrade cycle for iPhone 6S is on the slightly higher side that it experienced with iPhone 5S two year earlier.

Nevertheless, Apple launched the iPhone SE on March 31 this year to tackle the slowdown in sales. The iPhone SE is expected to attract customers due to a couple of reasons. First, it provides the customer with the latest technology with a more compact package, and second, a new entry point. Apple is focusing on the segment that aspires to own an iPhone but couldn’t quite stretch to the entry price of the iPhone. Thus, the addition of the iPhone SE in the iPhone lineup should create a strategic position for Apple to attract more customers to its brand. Apple is witnessing good customer response since the launch of, which is a good sign for investors.

In my opinion, iPhone SE with a new entry point will make a remarkable presence in the emerging markets such as India that is embracing more and more iPhone. For instance, Apple’s sale in India for the last reported quarter rose 56% year-over-year. In fact, its market share increased 29% at the end of the first quarter from the year-ago period. This growth suggests that Apple is outperforming its peers in India, which is a green flag for investors.

Service segment remains a tailwind

Apple continues to see an upward revenue trend for its service segment that generated $6 billion in the last reported quarter, representing an increase of 20% year-over-year. These robust service numbers are due to a continued high performance of the App Store that witnessed a whopping 35% growth on an annual basis. In fact, the App Store generated 90% more global revenue than Google Play in the March quarter, up from a 75% lead in 2015.

In addition, during the quarter, Apple improvised its music business that has now both a download model and a streaming model. With these upgrades, its music business has reached an inflection point after many quarters of decline, which is a positive sign for its investors. The music business has approximately 13 million paying subscribers at the end of the second quarter of 2016.

Apart from App Store and Apple Music, another promising product for Apple under its service business is Apple Pay. According to the management, “Apple Pay is growing at a tremendous rate, with more than five times the transaction volume of a year ago and 1 million new users per week. There are more than 10 million contactless-ready locations in the countries where Apple Pay has launched to date, including over 2.5 million locations now accepting Apple Pay in the United States, and more expansion of Apple Pay is coming soon”.

According to a research company eMarketer, the U.S. proximity mobile payment market could triple in 2016, growing from $8.7 billion in 2015 to $27.1 billion in 2016. Thus, this growing mobile payment market should provide a significant opportunity for Apple Pay to grow its customer base and improve its service revenue going forward.

Moreover, the company during the first quarter launched Apple Pay in China and a week before in Singapore. In fact, Apple is planning to launch Apple Pay in various Asian countries this year that should improve its revenue additionally going forward.

Conclusion

Although Apple is experiencing softness in the iPhone sales in the United States and China, it remains an attractive investment opportunity on the recent dip. Its market share in the Indian market is growing and at the same time the company unveiled iPhone SE series that should compensate for the drop in U.S. sales to an extent.

At the same time, the company has upgraded its iPhone 6S that should lead to a better sales numbers in the upcoming quarters. Also, its service business mainly App Store, Music, and Apple Pay are growing at a tremendous rate that should keep the momentum for Apple going forward.

![]()

![]()

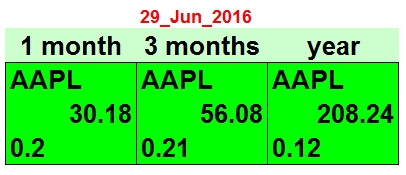

My bullish stance on Apple is resonated by I Know First’s algorithmic signals. I Know First uses an advanced state of the art algorithm based on artificial intelligence and machine learning to foresee market performance for more than 3,000 markets including stock forecasts, world indices, commodities, interest rates, ETFs, and currencies. The algorithm generates a forecast with a signal and a predictability indicator. The signal is the number at the center of the box. The predictability is the figure at the bottom of the box. At the top, a particular asset is identified. This format is standardized across all forecasts. The middle number indicates strength and direction, not a price target or percentage gain/loss. The bottom figure, the predictability, signifies a confidence level.

As seen from the above image, I Know First’s 1-year forecast is extremely bullish on Apple, which coincides with my outlook as well.