Total SA Stock Analysis: Solid Foundations for an Impressive Future

The article was written by Harry Chiang, a Financial Analyst at I Know First.

The article was written by Harry Chiang, a Financial Analyst at I Know First.

Total S.A. Stock Analysis

“My formula for success? Rise early, work late, strike oil.” Jean Paul Getty, Founder of Getty Oil Company

Summary:

- Despite Industry Problems, Total Displays Strong Finances

- Iran is Opening New Investment Opportunities

- Total SA is Taking its Work Global

- The Company Has Diversified for a Complicated Future

Background

Total finds its origins in France during the messy aftermath of World War I. It begins with Royal Dutch Shell proposing a partnership to then Prime Minister Raymond Poincare. Disillusioned with that idea, Poincare asked Ernest Mercier to create an entirely French oil company. With the support of ninety banks and companies, Mercier founded Total as the Compagnie Francaise des Petroles (CFP) in 1924. Total S.A. itself only first took form three decades later, in 1954. CFP introduced it as a downstream product, Total, brought to Africa and Europe. This eventually led to the company rebranding itself as Total CFP in 1985 as a response to the popularity of its gasoline brand. Finally, Total S.A. emerged in 1991. This was after the board listed it on the New York Stock Exchange. This was accompanied by the reduction of the French Government’s stake in the company from 30% to 1%.

Today, Total is one of the seven supermajor companies in the oil industry. Supermajors, or “Big Oil”, are the world’s seven or eight largest oil and gas companies. Total’s current business operations include the entire oil and gas chain, from crude oil and natural gas exploration and production to power generation. The company’s headquarters are in Paris.

The company divides its operations in to three primary segments: Upstream, Refining & Chemicals, and Marketing & Services. The Upstream segment deals with the exploration and production activities of the company in 50 different countries. Upstream produces oil or gas in 30 countries, and purchases, sells, and ships liquified natural gas (LNG). The Refining & Chemicals segment refines petrochemicals and is involved in trading and shipping crude oil and petroleum products. The Marketing & Services segment supplies and markets petroleum products, including aviation fuel, special fluids, LPG, etc. The company operates approximately 16,000 service stations and employs close to 100,000 people.

![]()

![]()

Despite Industry Problems, Total Displays Strong Finances

Despite having troubling earlier years, Total SA is currently doing well financially. It is in a good place to compete with other major oil and petroleum companies, and stands to grow more. This is made evident by the company’s financial reports.

Adjusted net operating income from the business segments was $2,767 million in the first quarter of 2017. This was a 47% increase compared to the first quarter 2016. Total attributes this increase to the improved contribution from Exploration & Production, which fully captured the benefit of higher hydrocarbon prices. Similarly, adjusted net income was $2,558 million in the first quarter of 2017, compared to $1,636 million in the first quarter of 2016, an increase of 56%.

Furthermore, adjusted earnings per share, calculated on the basis of 2,457 million fully-diluted weighted-average shares, increased by 49% to 1.01 dollars in the first quarter 2017 from 0.68 dollars in the first quarter of 2016.

In the first quarter of 2017, the Group’s cash flow was positive $3,907 million compared to a loss of $215 million in the first quarter 2016. Moreover, operating cash flow before working capital changes increased by nearly a $1 billion compared to a year ago. This was again due to the higher contribution from Exploration & Production.

Currently, Total continues to reduce its breakeven by cutting costs in line with the $3.5 billion savings target for the year and benefiting from project start-ups. In the Upstream, the Group maintains its production growth objective of more than 4% in 2017. In addition, in the Downstream, refining margins remain favorable going into the second quarter.

These 2017 results are building on already improved results from 2016. Last year, Total S.A. had revenues of $35,654.78 million and net earnings of $529.98 million. Gross margins widened from 2.18% to 2.47% compared to the same period last year, operating (EBITDA) margins were 15.87%, up from 10.66%. Hence, these strong reports indicate that Total S.A. is in a good place to continue to grow.

Iran is Opening New Investment Opportunities

Until recently, Iran was a very difficult investment prospect. Regulations and politics made it difficult to engage in the country’s resources and develop them. However, Total SA is currently in talks with Iran to develop part of the world’s biggest natural gas field in the next few weeks. Last year, Total and China National Petroleum Corp. signed a “heads of agreement” with National Iranian Oil Co. to develop phase 11 of the South Pars gas field. Upon time of signing, Total valued this deal at $4.8 billion.

For perspective, Iran has the world’s biggest gas reserves and is the third-biggest oil producer in the Organization of Petroleum Exporting Countries (OPEC). After Iran eased sanctions related to its nuclear program in January 2016, Total increased its oil production 33%. Thus, it is evident that Total’s new position in Iran gives it a good position to develop one of the highest potential projects in the oil industry. Total further stated that it is willing to pledge a further $1 billion in investment in Iranian gas fields.

Total SA is Taking its Work Global

As indicated by the Iran project, Total is in no way limiting itself to American fields. Nor is it limiting itself to a single country for development. In fact, Total SA is making major global moves with various international projects. These are expanding Total’s reach, influence and growth potential.

For example, in 2017, Total started up production from the Moho Nord deep offshore project in the Republic of Congo. This is considered the biggest oil development to date in the Republic of Congo. Total stated this project will contribute to the reinforcement of the cash flow of the Group and to its production growth. Moreover, Total is also establishing itself in South America. Total and Brazilian Petrobras have signed final terms of a $2.25 billion joint venture. This involves the sale of assets as well as stakes in oilfields and two thermal power stations. Total has also sanctioned the development of the first phase of the operated Aguada Pichana Este license in the Vaca Muerta shale play in Argentina. This is accompanied by the Group increasing its interest in the license from 27.27% to 41%.

Other projects currently include Total and SONATRACH’s agreement which allows the two to expand their partnership through new upstream contracts in Algeria. Total and SOCAR have also signed an agreement establishing the terms for the first phase of production of the Absheron gas and condensate field. In addition, in February 2017, Total signed an agreement for the sale of stakes and the transfer of operatorship in various mature assets in Gabon to Perenco. This was a major Total transaction valued around $350 million before adjustments.

This is not all to say that Total is not focusing on the growing oil market of America as well. For example, Total is launching a multi-billion-dollar petrochemical joint venture in Texas. Total is planning to provide the initial $1.7 billion for the operation. The venture would start in 2020 and create at least 1500 local jobs.

The Company Has Diversified for a Complicated Future

There has been much speculation recently as to the future of the oil and gas industry. Many are dubious of its potential to go much further in our complicated energy situation. Total SA, unlike many energy companies, is unusually dedicated to renewables. In 2016, the Group presented a proposed new organization to employee representatives. This included the creation of the Gas, Renewables & Power Segment. This Segment will spearhead Total’s ambitions in the electricity value chain by expanding in downstream gas, renewable energies and energy efficiency. Total also dedicated itself to the creation of a new Total Global Services segment. The company created this to sustainably improve efficiency across all business by globally pooling support services.

Furthermore, the corporate headquarters aimed to refocus on strategic functions. In addition to the current finance organization, two new divisions will be created: People & Social Responsibility, and Strategy & Innovation. These will be focusing on improving Total’s commitment to environmental development and responsibility.

Total’s current ambition is “20% low-carbon businesses in 20 years’ time”. The current CEO has stated that this means that renewable energies along with energy storage and energy efficiency should represent 20% of the company’s portfolio in 20 years’ time. This is a representation of 20% of Total’s current $130 billion assets, a significant sum.

In addition, Total is also making moves in terms of acquisitions in the renewable energy industry. The company recently announced that is buying Lampiris and the Saft Group. Lampiris is Belgium’s third-largest supplier of natural gas and renewable power. This deal with Total, which has a value of $224 million, allows Total to expand its gas and renewables assets. It also allows Total to be further involved in the residential electricity market. This is paired with the Saft Group’s manufacturing of batteries for electricity storage.

It would be remiss to forget Total’s already impressive renewables involvement. In 2011, Total purchased 60% of the solar company SunPower for $1.4 billion. This is expected to bring in $3.2 billion in revenues this year. Furthermore, the company also plans to transform the La Mede oil refinery into a biofuel plant.

Although these renewable options do not currently represent a massive portion of Total’s revenues, they are poised to be very profitable in the future. It is important to note that it is not just Total’s actual acquisitions, but also its dedication to the vision of renewable energy which make this such a powerful and unique growth engine.

Conclusion:

Perhaps nothing noted here particularly strikes as an explosive growth indicator. However, Total SA is in a very good position to keep steadily plugging on in a volatile industry, a more valuable factor than many other similar companies can lay claim to. Total SA is slowly developing its strong foundation so that it can grow in the future – this is a long-term game for the company. It is already demonstrating that its planning has been delivering results and we expect Total SA to continue to do well. We are maintaining a bullish forecast of the stock. I Know First’s algorithm forecast the stock as a long term investment.

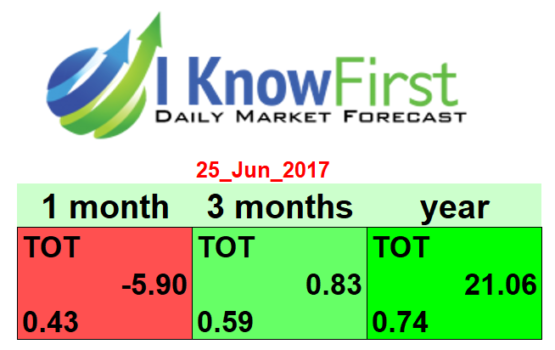

Current I Know First Forecast for TOT:

Below is the latest forecast I Know First algorithm released as of today on June 25, 2017. Although the algorithm predicts a decrease in the short-term, we can see that in the long-term, I Know First still rates Total as bullish and as a buy. As mentioned before, this is a long-term investment, as Total is making moves well in to the future, built on its foundations of today.