Stock Market Forecast for 2017 Based on Artificial Intelligence

This article was written by David Shabotinsky, a Financial Analyst at I Know First, and enrolled at the undergraduate Finance program at the Interdisciplinary Center, Herzliya.

This article was written by David Shabotinsky, a Financial Analyst at I Know First, and enrolled at the undergraduate Finance program at the Interdisciplinary Center, Herzliya.

Stock Market Forecast for 2017

Summary

- Past Global performance from the financial markets including equity, commodity, and forex markets

- I Know First’s self-learning algorithm’s 2016 performance in underlying assets found in financial markets

- Goldman Sachs Group, Deutsche Bank, and Vanguard’s 2017 global investment & economic outlook

- I Know First’s algorithmic indice forecasts for 2017 and forward-looking macroeconomic environment analysis

“In the business world, the rearview mirror is always clearer than the windshield.”

– Warren Buffett.

Past Systematic Financial Market Performance For 2016

Though many say that hindsight is 20/20, in the financial arena, empirical evidence and historical performance continue to be one of the best ways to evaluate an investment opportunity set.

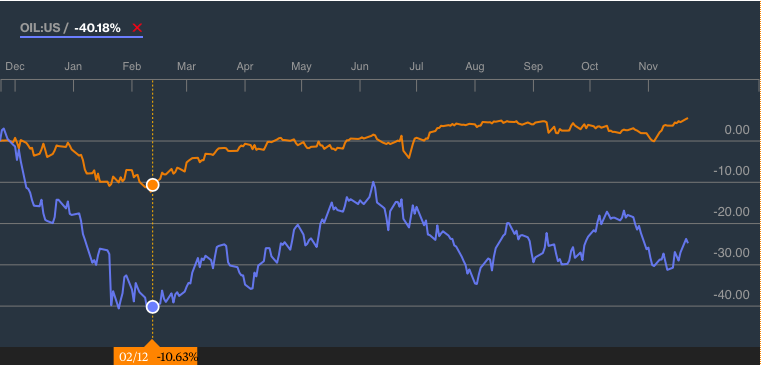

Over the past year since the beginning of 2016 many systematic events had occurred that caused many market predictors to be wrong in the predictions. Though many had anticipated a global recession, investors had shown reinforced confidence as shown by summer 2016 having low volatility. During Q1 2016, equity markets had taken dramatic downturn mainly due to a fall in oil prices. Oil prices though are now beginning to slightly recover slowly, in the beginning of the year crashed down to $25 a barrel causing U.S. equities overall to dip very low.

(Source: Bloomberg)

Though oil has slightly recovered a mix of lower than expected demand, or global consumption; and a continual oversupply of global output for oil (crude oil) has kept prices depressed. Historically, the summer is a time for high demand for oil as households travel and enjoy other leisure activities to amount to a higher consumption. Though many O&G companies, such as MLPs, have been battered since oil’s decline in 2014, many are continuing to survive by selling assets to pay off high debts along with cutting operational expenses.

Moving towards Q2 2016, Brexit caused massive market panic with the market betting on a no-vote, though now inflation seems to be picking thanks to the Bank of England governor mark carney who scrapped an interest rate increase and had almost doubled 2017 economic outlook forecast for a post-Brexit world in the UK, later he cut interest rates from 0.5pc to 0.25pc which had helped the sensitive housing market in the UK rise along with consumption in the UK. Moving into Q3 2016, the pound had experienced large amounts of volatility as a result of high uncertainty, though it has mainly stabilized now due to increasing consumption and inflation, here we see the volatility.

Commodities During 2016

Gold prices rose significantly as investors had worrisome expectations and there was high uncertainty thus rose to record highs. Additionally, central banks around the world, specifically, the Fed, have not been raising interest rates in order to spur inflation thus increasing investments into an inflation deterring asset such as Gold, which is used as a safe haven against inflation.

(Source: Bloomberg)

Though China has consumed less oil than expected other commodities such as Steel have seen a huge rebound with higher than expected consumption coming from china and other emerging markets around the world, though oil productions are slowly being capped to reduce supply with a peaking and stagnating global demand OPEC is still moving in a slow direction to a course of action.

Global Monetary Policies During 2016

Over the past year investors had expected monetary policy to implement a contractionary policy with a rise in interest rates, and while the Fed is expected to close 2017 with an interest rate increase, thus far, not enough positive economic data has helped support their conviction to increase rates at hand. Additionally, Japan, which has for a while now been trying to increase rates has now chosen to continue with negative interest rates and beginning to buy more bonds with the central bank to further help spur inflation by lowering the yen pegged against the USD. Additionally, the Eurozone maintains a slumped growth expectations, which are feuled as a result of a migration crisis, a continual Brexit uncertainty, PIGGS nations underperformance, and ECB’s failure to spur high inflation using negative interest rates.

U.S. Elections Amounting Volatility

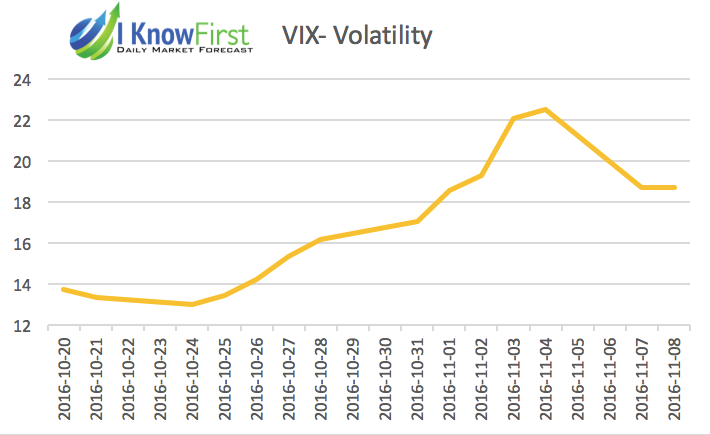

The summer of 2016l, had light volatility as investors had been reassured for not having a global recession due to global central banks actions post-Brexit. Though most investors had expected financial markets to dramatically fall with a Trump victory, considering the market had overall been betting on Clinton victory which had been represented by a large uptick in volatility (VIX), weeks before the election and with the S&P falling prior. Investors saw S&P 500 futures fall in the beginning and then dramatically increase overall for the next coming days specifically from U.S. industrial firms such as steel companies and the financial industry with expectations of deregulation from the new administration. click here to read how I Know First had successfully forecasted and navigated though this mass volatility prior and post U.S. elections.

Forward Looking 2017 Goldman Sachs Outlook

Over the past week on November 17th, 2016, Goldman Sachs Economic Research department had sent to its clients their top ten ‘themes’, or macroeconomic outlook for 2017 titled, “Top Ten Market Themes For 2017: Higher growth, higher risk, slightly higher returns.”

With global GDP expected to be reached at around 3-3.5% during 2016, the outlook for 2017 essentially maintains slight growth and upside overall, with the main opportunity sets in emerging markets. Furthermore, the team strongly believes, along with most investors, that the Fed will, in fact, raise interest rate levels during December 2016, along with three more times throughout 2017. High interest rates are able to counter inflation in the economy, as it depresses the GDP by lowering investment and thus snowballing to a lower consumption. This main relates to firms and households having a higher alternative investment (higher opportunity cost) by putting away into interest rate bearing instruments. The reason why the Fed would do this is that there two main objectives to control and stabilize are employment/unemployment and inflation. With output and employment reaching its full potential (full-employment rate), Trump’s infrastructure and fiscal spending would increase inflation.

This is the firm’s forecasts for both major currencies and indices such as the S&P 500 Index.

Overall, expected returns in the financial markets, specifically for the equity market has become overvalued in relation to historical standards, and thus it will be hard to generate high returns during such times. However, GDP and economic growth could rise during 2017, since the declining working age population is as bad as was expected and is even starting to slowly reverse course.

The main highlight points for 2017 forecasted by Goldman Sachs are:

- Expected returns: Only slightly higher

- US fiscal policy: A pro-growth agenda

- US trade policy: Concerns are likely overdone

- EM risk: ‘Trump tantrum’ is temporary

- Trump and trade: Hedge with RMB

- Monetary policy: Focusing the toolkit on credit creation

- Corporate revenue growth recession: Signs of inflection

- Inflation: Moving higher across DM

- The next credit cycle: Kinder and gentler

- The ‘Yellen Call’ 2.0: Now with ‘contingent knock-in’

Overall, Goldman Sachs believes that though a Trump administration’s outlook on the economy is still uncertain, it will likely be in line with a republican pro-trade agenda. Additionally, China and U.S. trade relations are likely to continue as in the past and are heavily blown out of proportion.” Our forecasts ($/CNY at 7.30 in 12 months) call for a depreciation that is well beyond forward market pricing, thereby implying positive gains even accounting for the negative carry,” the strategist writes.” And beyond the usual reasons for wanting to hedge exposure to ‘China risk,’ we think it will also hedge the risk of a ‘Trump trade tantrum.'” Emerging markets in general present a great opportunity for investors as the current negative outlook due to Trump is as well only temporary.

Deutsche Bank Capital Market Outlook

Though Goldman Sachs has moved to the idea that markets are risk from overvaluation, Deutsche Bank believes that global political risk may be the strongest indicator for the investment world for 2017. In Europe, the Italian referendum is over and a new government is emerging with high expectations to for a more populist government to emerge with a similar mindset as to that of politicians who had proposed Brexit. Germany, Netherlands, and France, are expected to have elections for a new government in the coming months. Large parts of the population, especially the middle class, are being swayed by extremist on both political spectrums after feeling ignored and underhanded by globalization and as a result of an immigration policy that has further induced fears. As a result, the bank expects a decrease of 0.5% in growth to just 1% for 2017.

Moving towards the U.S. markets, Deutsche Bank expects a more modest growth of around 2.3%, if the economic policies of tax reform, deregulation, and stronger fiscal spending are implemented with the new administration. Additionally, U.S. sectors that will likely benefit from Trump’s economic policies are the financial sector and healthcare sector, due to expected reforms that will loosen regulation in those areas. Financial sectors will furthermore be able to expand their margins from an interest rate rise during 2017. The bank does expect the Fed to beginning a modest increase to interest rates, however; other central banks such as the ECB will likely continue an expansionary policy of bond buying programs. Therefore, the dollar will continue an appreciation, specifically against the euro, as a result of a higher capital inflow.

Both these two sectors, along with other fiscal spending i.e. U.S. infrastructure, has strengthened Deutsche Bank positive outlook in regards to the S&P 500 Index. The bank expects a further increase in the price level during 2017, to a level of 2350 points by the year-end.

Vanguard 2017 Global Investment Outlook

Led by Vanguard’s Global Chief Economist Joe Davis, the firm maintains that certain challenges continue to arise for the investment cycle in 2017; though they are slightly more optimistic than Goldman Sachs. Overall, the firm maintains that a historical slow recovery from the global recession will continue to put pressure on inflation and growth. This is added to the fact that the Fed will likely increase interest rates, practicing a contractionary policy in one of the world’s largest economies. The firm does not expect the global economy to reach a stagnation level or that of Japans.

With regards to global monetary policy, the firm expects the Fed to raise rates to a maximum level of 1.5% benchmarked rates. However, they do expect that the ECB and BOJ to continue with quantitative easing throughout 2017. Furthermore, Vanguard has forecasted a more bearish outlook on China’s growth, as the country continues to tackle how to prevent a serious capital outflow; yet still being able to lower interest rates and exchange rates. China’s state-owned enterprises continue to be a benchmark indicator set on how well the government reforms will be and its impact on the economy.

In terms of global investing, the over valuation of stocks into what many may call reaching a bubble peak, is as well fueled by low interest rates which are expected to be done away with therefore very hard to justify a high opportunity. Though they maintain a more optimistic outlook than Goldman Sachs, on equity returns with a modest 5%-7% in the medium run, they do admit to a poor growth environment can hurt returns as well as the necessity to adjust to a low rate environment when forecasting returns.

I Know First 2017 Macro Economic Outlook

I Know First, Ltd. is a financial technology company that provides daily investment forecasts based on an advanced, self-learning algorithm. The Algorithm was developed by Dr. Lipa Roitman, a scientist with over 20 years of experience in the field, and who now leads our Research & Development team to further develop and enhance the algorithm.

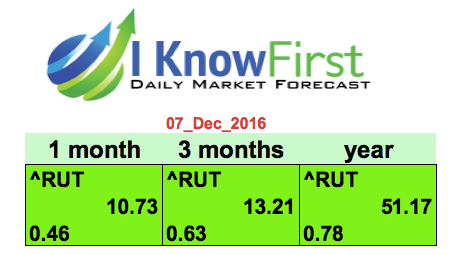

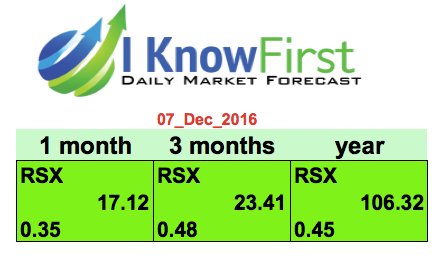

Looking forward into 2017, the algorithm currently forecasts for a rise in the Russel 2000 Index (RUT) for 2017, while forecasting a mid-term rise in the S&P 500 Index. Though the algorithm does predict a slight rise in the equity market, the main opportunities lie in small cap stocks as represented by the RUT. The reason is that even though wall street has set its hopes on deregulation and higher fiscal stimulus spending, global financial markets are highly overvalued. Therefore, the more prominent opportunities sets, to garner high returns, will need to be sought out from riskier investment in small cap firms. Additional opportunity sets may arise from emerging market economies, specifically that of Russia, as tracked by RSX. This due to the fact that Russia is slowly exiting it’s economic recession fueled by sanctions and an oil price crash. Currently, many reputable multinational corporations, such as Nestle. Additionally, analysts are expecting a warmer U.S.-Russian relationship under a Trump administration.

*RUT has a 1 year signal strength of 51.17 and a predictability indicator of 0.78. Below is A detailed explanation of the signal strength and predictability.

Furthermore, in regards to large cap firms that represent the S&P 500 Index, they have already shown slower growth over the past year with overall falling corporate earnings. A huge driver for a growth strategy for ones that are continuing to grow is M&A with cheap debt. Their opportunity costs will only increase with a highly anticipated rate hike from the Fed. Small cap firms, however, are still able to grow as they generally have not reached their full potential, maturing stage.

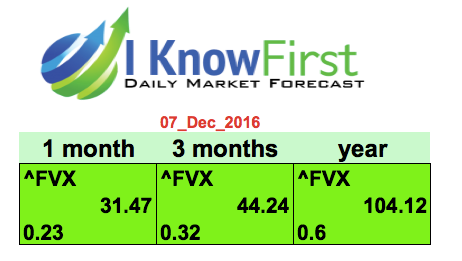

Additionally, with expectations for a Fed rate hike increasing by the day, I Know First’s self-learning algorithm has a bullish outlook for treasury yield 5 years (FVX) for the next year. This would put pressure on the U.S. economy in a negative aspect and drive the price down for the 5-year treasury bill. As there is an inverse relationship between a bond yield and its spot price, the lower confidence investors have in the U.S. economy the higher likelihood they will will opt to store investments in safe havens such as bonds. The capital inflows will likely cause a further appreciation of the U.S. dollar, which will put pressure on multinational corporations based in the U.S. The reason is because much of their revenues are based on foreign currencies, while the costs are in dollars. Therefore, depending on their sensitivity to exchange rate risks as function of one divided my profit margins overseas, will impact earnings.

I Know First Algorithm Heatmap Explanation

The sign of the signal tells in which direction the asset price is expected to go (positive = to go up = Long, negative = to drop = Short position), the signal strength is related to the magnitude of the expected return and is used for ranking purposes of the investment opportunities.

Predictability is the actual fitness function being optimized every day, and can be simplified explained as the correlation based quality measure of the signal. This is a unique indicator of the I Know First algorithm, allowing the user to separate and focus on the most predictable assets according to the algorithm. Ranging between -1 and 1, one should focus on predictability levels significantly above 0 in order to fill confident about/trust the signal.

Conclusion

Though over the past year, commodities have greatly rebounded and gold has outperformed expectations, investors need to be wary moving forward and closely examine their given investment portfolio and options at hand. Through neural networks, deep learning, and artificial intelligence; I Know First’s algorithm had been able to forecast these rebounds and continues to help investors achieve superb alphas above the S&P 500 Index as its benchmark. With Trump’s uncertain presidential election looming ahead and the Federal Reserve future meetings, many economic questions are still unanswered. Goldman Sachs still has a bullish outlook on the global equity markets, with emerging markets able to better capture opportunity sets for investors. Additionally, Goldman’s market predictions are overall in-line with I Know First’s algorithmic forecasts for 2017, as shown above. Investors should follow suite with strong conviction in the financial markets, and should closely examine small to mid-market firms in the U.S. and in emerging markets to find great opportunities moving forward.