Go Long On Lululemon, Stock Is Above Under Armour

This article was written by Julia Masch, a Financial Analyst at I Know First.

“A big reason athleisure is colonizing stores is that the clothes are comfortable, with form-controlling fit on many core styles. Brands at all price points have something to offer, from traditional athletic names to specialty chains to high fashion labels, along with a laundry list of new entrants.”

– Elizabeth Holmes, Wall Street Journal

Known for starting the athleisure trend and making yoga pants popular everyday attire, Lululemon Athletica (NASDAQ: LULU) has had a great year. After only hitting $90 for the first time in April, the stock skyrocketed to above $120 following the release of its phenomenal Q1 earnings report.

Whereas Lululemon has only recently become a force to be reckoned with, Under Armour (NYSE: UAA) has been a mainstream competitor in the athletics apparel market for years. However, the company is not as strong as it once was. So which athletics retail stocks are worth buying?

Highlights:

- Solid Q1 2018 for Lululemon and Under Armour

- What’s next for both companies?

- Current I Know First Forecasts

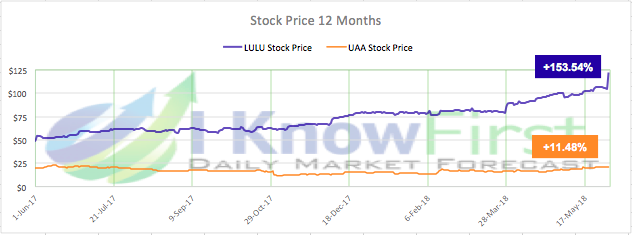

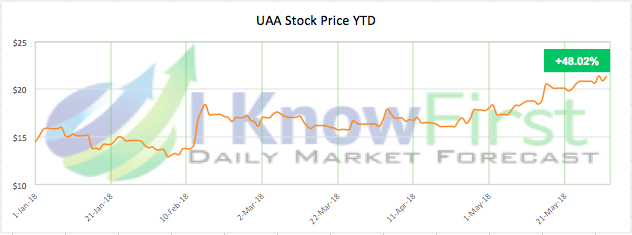

From first glance, it appears as though Lululemon has been outpacing Under Armour with gains of over 150% in comparison to an increase of only 11.48% for UAA over the last 12 months. However, in the shorter term, the stocks have increased at a closer rate with 55.48% and 48.02% increases YTD for Lululemon and Under Armour respectively.

Lululemon has been continually growing from a niche store for yogis to a strong athletics apparel competitor. Meanwhile, Under Armour had a tough 2017 and is now beginning to rally once again.

No Negatives: LULU’s Strong Q1

According to the Q1 2018 earnings report, Lululemon surpassed expectations in almost every facet of its business with revenue, earnings per share (EPS), comparable sales, and gross margin all increasing, leading the company to believe it remains on track to hit its revenue target of $4 billion by 2020. After the earnings report on June 1, LULU closed at $122.19, a new high.

Total revenue grew 25% to $650 million for the quarter with a 53.1% gross profit of $344.7 million which was an increase of 270 basis points YoY and was the result of a 120 basis point improvement in product margin and exceeded analyst estimates of $618 million. The increase in revenue led to $0.55 EPS, well above the expected estimates of only $0.46.

LULU Quarterly Revenue and Earnings (Source: Yahoo Finance)

Additionally, product margins improved by 380 basis points thanks to strategies increasing the efficiency of sourcing and distribution. There was also a decrease in selling, general, and administrative (SG&A) expenses which contributed to the better product margins. On top of all of these changes, combined comparable sales (comps) also increased by 19% thanks to same store comps rising by 6% (a 7% increase YoY) along with e-commerce growth of 60%.

Looking Ahead At Lululemon

Looking forward, the company expects to continues its growth trend. The company raises its expectations for FY 2018 revenue to $3.04-$3.075 billion from $2.985-3.022 billion and consequently raises EPS expectations by $0.10. Revenue for FY 2017 was only $2.60 billion, so these numbers show the company is capable of achieving the goal it set in 2016 to increase revenue to $4 billion.

Online Expansion

Lululemon’s success is not only evident in the strong numbers in Q1, but also in their strategies for continued growth. Online business was a large component of the almost 20% gains in combined comps. These online sales are integral to LULU’s continued success as mall traffic continues to fall. The company has added new processes to streamline online shopping on their website and will continue to do so in Q2 and Q3. New shipping choices now give consumers the option to ship an item from stores so they receive it faster or to buy online and pick up an item in store. Lululemon’s digital team has brought in new traffic as well as doubled the company’s already large mail file. Moreover, the sales team has been able to improve targeting capabilities and improve the online experience for guests with better landing pages, content, navigation, and more. As a result, and the company has begun seeing greater traffic levels and more returning guests and there has been a 50% increase in transactions made by returning guests. What is also important to note is that over 30% of the new customers the company is attracting are men which is allowing Lululemon to gain a greater market share in men’s athleisure. Lululemon will continue to improve the online shopping experience for its customers and expects the online shopping momentum to continue into Q2.

Physical Expansion

Lululemon is not only expanding its online prospects, but is also opening new stores throughout America and new markets. The company currently runs over 400 stores and has opened up 48 new stores since Q1 2017 and increased store square footage 14% over this time. Additionally, Lululemon has been entering new markets and broadening its horizons in Asia and Europe. In Asia, combined comps were over 50% with particularly strong results in China, where the company plans to continue opening new stores in the upcoming quarters. LULU also looks to capitalize in Korea and has recently opened its third and fourth stores in Seoul and hopes to introduce e-commerce in the country soon. Lululemon expects to open 15-20 new stores in Asia in 2018, which, combined with another new market for e-commerce, will increase revenue. The company will also work on increasing its reach in Europe where it has already seen strong growth. New Lululemon stores recently opened in Berlin, Frankfurt, and across the UK. Lululemon has been diligent about researching cultures and trends in these countries to ensure its best chance for success in these new markets.

(Source: Wikimedia Commons)

The Hunt For a CEO

In February, Lululemon’s CEO, Laurent Potdevin, left the company abruptly after undisclosed charges of misconduct. Since then, the company has been without a CEO and is in the process of searching for a replacement. Lululemon will soon take this search to the next step from finding the right candidates to interviewing and selecting one. The lack of a CEO is the only foreseen issue for the company; however, the company has a competent board that should pick a good candidate and the Q1 results have shown Lululemon is able to thrive in the short term despite the absence of a CEO.

Under Armour

Under Armour has not had a bad year, however, the company is not the power house it once was: since hitting its all time high in September 2015, UAA has sunk over 40% and does not produce the same 20% sales growth it once had every quarter.

However, the company is not throwing in the towel. After a difficult 2017, Under Armour’s stock is beginning to bounce back and has outperformed the market YTD with gains of 48.02%.

Under Armour’s Average Q1

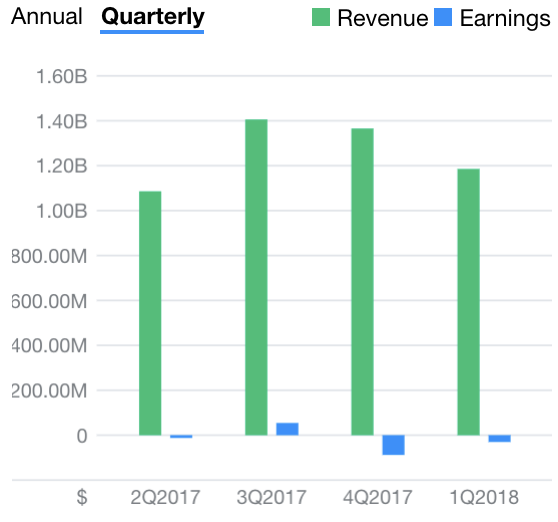

While Under Armour’s Q1 2018 results were good, it certainly did not compare to Lululemon’s exceptional earnings during the same time period. Under Armour had adjusted EPS of $0, which did beat expectations of a loss, but still are much less than LULU’s EPS of $0.55. Additionally, while revenue did increase 6% to $1.2 billion, revenue growth has slowed over the past quarters and does not compare to the 20% revenue increase UAA posted at its prime. Revenue in North America was relatively flat; however, international revenue was up 35% in Asia Pacific, 23% in Europe, and 21% in Latin America. While these international numbers are promising, North American revenue still makes up 73% of global revenue.

Quarterly Revenue and Earnings for UAA (Source: Yahoo Finance)

GAAP gross margins also declined 120 basis points to 44.2% and excluding restructuring costs gross margin was 44.8% due to markdowns to clear inventory. Earnings for Under Armour have been negative for the last 2 quarters and the company looks to improve this in the future.

What’s Next for Under Armour?

Under Armour expects revenue growth in the low single digits for the full year and adjusted EPS of of $0.14-0.19. Additionally, in other aspects, the company expects momentum from Q1 to continue into the next quarter. Under Armour has also experienced a boost from strong earnings from retailers that sell its products. For example, following a strong earnings report for Dick’s Sporting Goods, Under Armour’s biggest customer, the UAA price increased a few percentage points. Kohl’s also attributed growth in athletics apparel revenues to its partnership with Under Armour. Additionally, Under Armour is working on understanding its customer base better so that the company can tailor a better shopping experience. The company believes it can capitalize on health conscious consumers and has acquired MapMyFitness and has also been working on developing wearable technology which has finally started to impact sales. Under Armour’s new HOVR line of sneakers, which includes tracking and other digital features, has sold out and shown strong demand. The company’s President, Patrik Frisk, also just invested $500,000 in UAA shares, showing his vote of confidence in the company.

![]()

(Source: Wikimedia Commons)

Inventory Issues

In the past quarter, Under Armour’s inventory increased 27% to $1.1 billion. This amount of inventory would normally take about a year to clear (and that is if it were current). In the past Under Armour has sold apparel to clearance stores, but this degraded the semi-premium brand image UAA once maintained. Alternatively, Under Armour can continue making markdowns to decrease inventory, but this will also decrease gross margins, which the company should be increasing to increase growth. The company expects Q2 2018 inventory growth to be lower at 20%, but the company should accelerate clearing its current inventory too. In comparison, Lululemon inventory is only $373 million, but is comprised of very current clothing that the company expects to sell with minimal markdowns.

Technical Analysis

Lululemon is currently trading above its 50 day (light purple) and 200 day (dark purple) Simple Moving Averages (SMA) which indicates a bullish trend for the company.

Stock Price and 50 + 200 Day SMA for LULU Over 1 Year (Source: Yahoo Finance)

That being said, the company’s 14 day Relative Strength Index (RSI) is ~90 indicating it is overbought, which is the result of the massive quantity of trading following the release of the company’s extremely strong Q1 earnings report.

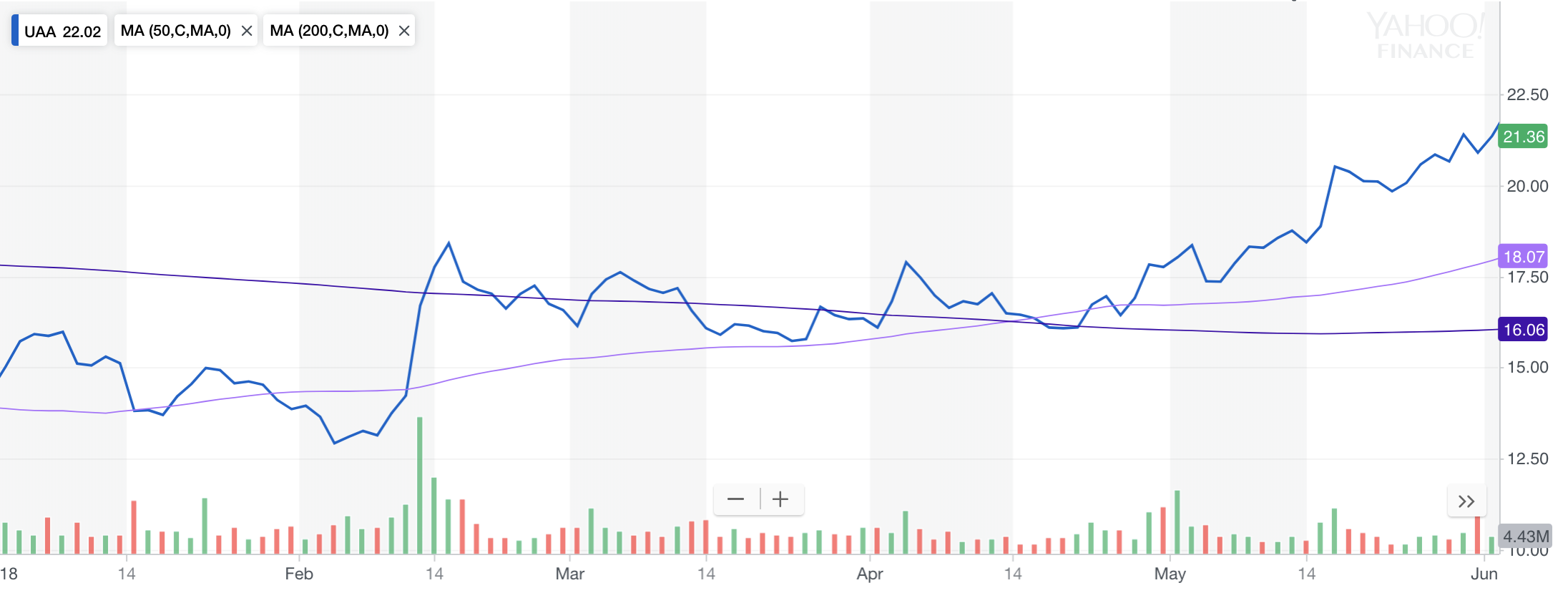

Stock Price and 50 + 200 Day SMA for UAA Over 1 Year (Source: Yahoo Finance)

Under Armour is also trading above its 50 day (light purple) and 200 day (dark purple) SMAs. This shows that UAA also has a bullish momentum going forward. Additionally, there was recently a golden cross in which the 50 day SMA overcame the 200 day SMA, which means the future may still be bright for Under Armour. UAA’s RSI is also ~69, very close to the boundary of being overbought.

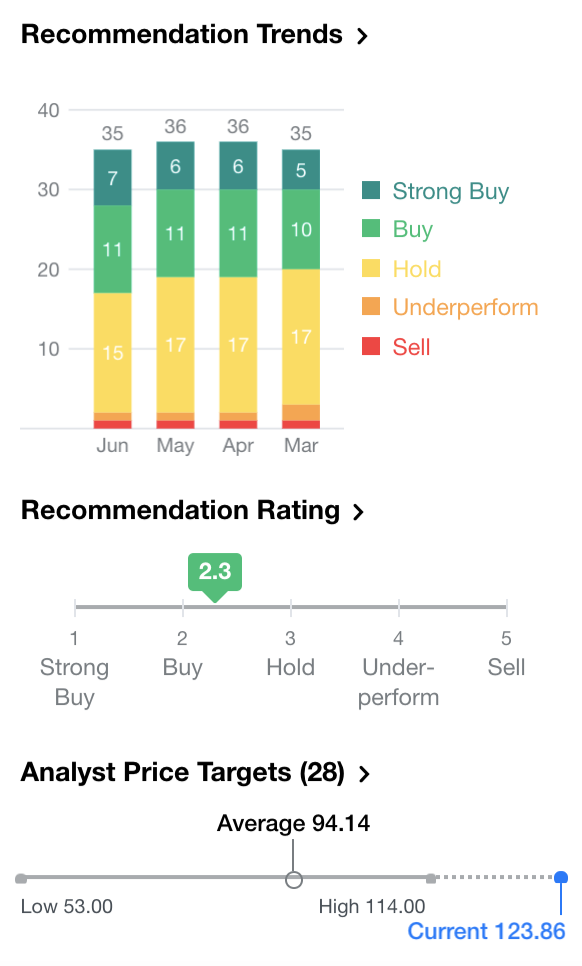

Analyst Recommendations

Lululemon

Lululemon currently has a recommendation rating of 2.3, with a little more than half of analysts opting to “Buy” or “Strong Buy” LULU. Additionally, the stock is currently high above many analysts’ price targets.

(Source: Yahoo Finance)

Following the release of Lululemon’s Q1 2018 earnings report, many analysts have increased their price targets for LULU: Citigroup raised estimates from $90 to $112, JP Morgan from $111 to $133, Credit Suisse from $105 to $125, MKM Partners from $120 to $128. Many other analysts followed suit and have increased their estimates by ~$20.

Under Armour

Meanwhile, predictions for UAA are not as positive with a recommendation rating of 3.1 and the majority of analysts choosing to hold the stock. Additionally, more analysts chose “Underperform” or even “Sell” in comparison to Buys (Regular and Strong).

(Source: Yahoo Finance)

Under Armour is also trading above the average analyst price target, however, it is still within the range of analyst estimates. Deutsche Bank recently upgraded UAA from a Sell rating to a Hold.

I Know First Forecasts

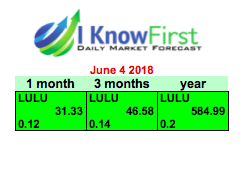

Current I Know First Algorithm Bullish Forecast For LULU

The I Know First Algorithm currently has a bullish prediction for Lululemon with signals of 31.33, 46.58, and 584.99 for the 1 month, 3 month, and 1 year time periods respectively. The extremely strong signal of above 500 for the 1 year time horizon indicates that it is logical to go long on Lululemon.

Current I Know First Algorithm Bullish Forecast For UAA

The I Know First algorithm also has bullish predictions for Under Armour. The algorithm predicts a signal of 82.38 over 1 month with a predictability of .42, a signal of 129.04 over 3 months with a predictability of .6, and a signal of 107.36 over 1 year with a predictability of .69. The predictability indicators for UAA sare stronger than those LULU. Under Armour has stronger bullish signals for the shorter time frames of 1 and 3 months, but a lower bullish signal over the 1 year time horizon.

Conclusion

Both Lululemon and Under Armour are strong athletics apparel companies, but Lululemon is a better buy. While Under Armour is moving away from its last heyday in late 2015, Lululemon is only growing and getting bigger and hit its all time high on June 1, 2018. Additionally, Lululemon has a clear strategy for continued growth by expanding its online and international presence whereas Under Armour is already such a force that further expansion may lead to cannibalization. I expect Under Armour to continue slowly and steadily climbing in the short run, but in order to see revenue growth return to what they once were the company will need to adapt its strategies and decrease its inventories. At the moment though, Lululemon is slightly overpriced and overbought due to the surge following Q1 earning release, so it may be wise to wait until the price dips before buying in. The technical analysis further confirms my bullish prediction for both stocks. In line with the current I Know First Forecast, UAA may be a better stock in the short term while LULU drops to a less extreme price, but it is worth it to go long on Lululemon.

Past I Know First Success With LULU and UAA

In this bullish forecast sent to subscribers on December 20, 2016, the I Know First Algorithm gave Lululemon strong bullish signals over the 1 month, 3 month, and 1 year time horizons.

In accordance with the high signal of 116.41 and high predictability of .5 that the I Know First Algorithm predicted for the next year, the stock rose 13.74%.

The I Know First Algorithm has also had success with Under Armour forecasts in the past. The machine learning algorithm gave a 3 day forecast on February 12, 2018 for its top 10 stocks package which included Under Armour. Over the following days, UAA increased by 33.89%.

Current I Know First subscribers received this bullish UAA forecast on February 12th, 2018.

Subscribe to I Know First’s Daily Market Forecast

How to read the I Know First Forecast and Heatmap

Please note-for trading decisions use the most recent forecast. Get today’s forecast and Top stock picks.