Netflix Stock Forecast: Why You Should Avoid Investing In Netflix Right Now

The article was written by Motek Moyen Research Seeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

The article was written by Motek Moyen Research Seeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

Summary

- Netflix has 137.1 million subscribers.

- This can grow to 150 million next year if Netflix goes big on marketing a cheaper mobile-only subscription plan.

- There’s probably more than 100 million potential customers who can only afford to pay $5 or less per month.

- However, there’s low margin in providing $4/month subscription plan. Netflix is spending more than $10 billion/year in original content.

- NFLX has bearish algorithmic market trend forecasts. It might be prudent to dump the stock now while it still trades above $280.

The stock price of Netflix (NFLX) has a 6-month performance of -24.10%. Further, NFLX’s current price of $282.65 is more than 30% lower than its 52-week high of $423.21. The bearish emotion over Netflix is due to rising competition in the subscription video on demand (SVOD). The perception now is that Apple (AAPL), HBO Go/HBO Now, Hulu, YouTube Premium, Amazon (AMZN) Prime Video, and Disney (DIS) are now hampering Netflix’s growth.

Now that Apple’s iPhone unit sales are stagnating, it will be aggressive in growing its paid streaming music/video streaming service. The very bearish forecasts from I Know First are all shouting it’s time to take profit on your NFLX holdings. Selling while this stock is trading above $280 is the right call. There’s no near-term catalyst that can boost this stock to above $300.

Netflix stock is with 112.67 return in 1 year since with a good agreement with this bullish forecast.

I believe Netflix still has the momentum to reach 150 million subscribers by Q1 2019. However, the rise of regional streaming firms like iFlix, Hooq, and Viu is another major headwind for Netflix in Asia.

(Source: Statista)

(Source: Statista)

Netflix had around 125 million subscribers early this year. It ended Q3 2018 with 137.1 million. However, many suspect that this double-digit annual subscriber growth rate cannot sustained for long. Aside from regional SVOD rivals, the growing internationalization of HBO, DisneyLife, and Amazon Prime Video services is making it harder for Netflix’s expansion outside North America.

Netflix has a massive 61% market share in North America, and 68% share in Latin America. Unfortunately, Amazon Prime is giving Netflix a tough fight in Asia Pacific and Europe. On a global wide basis, Netflix’s share is 37% and Amazon Prime Video, 20%. Amazon Prime is available in my country for 150 pesos per month ($2.88/month), but it requires a Globe mobile postpaid plan. Pretty soon it will be available for 450 pesos ($8.65) for non-Globe phone subscribers.

(Source: Statista)

(Source: Statista)

Rising Competition Is Forcing Netflix To Desperate Measures

Netflix’s ongoing test of a cheaper mobile-only plan in Malaysia is an act of desperation. The mobile-only (offered in SD resolution only) package costs $4, half of the regular monthly fee in Malaysia. This sub-$5/monthly plan can help Netflix boost its current 78.6 million number of international subscribers.

On the other hand, this mobile-only plan of Netflix could be easily exploited. It is easy to wirelessly mirror display a Netflix video stream from a smartphone/tablet to a large-screen TV/PC monitor. This loophole further adds to the low margin disadvantage of offering a $4/month plan.

On a brighter note, Netflix can further increase its number of subscribers among the mobile-only video binge watchers. For the past few years, manufacturers keep coming up with bigger smartphones with 5 to 6.8 inches display sizes. Many people now prefer smartphones with displays larger than 5 inches. This trend is tailwind for Netflix’s cheaper mobile-only subscription plan. An ordinary user will find it satisfactory to watch SD (standard definition) 480p Netflix movies on a 5 or 5.5-inch display.

Hitting 200 million subscribers by offering a mobile-only plan is a valid tactic for Netflix to stay ahead of Disney, Hulu, HBO, and Apple.

The Downside of Chasing Subscriber Count

A cheaper, mobile-only monthly package can derail Netflix’s improving operating margins. Netflix needs better profitability to recover the billions of dollars it spends on producing original content. It was reported that Netflix was spending around $13 billion on original content this year. This annual budget could grow to $22 billion by 2022.

Netflix’s low net margin (averaging less than 7% for the past 5 years) will eventually cause investors to lower the company’s valuation.

(Source: Finbox.io)

(Source: Finbox.io)

Compared to its sector and industry peers, NFLX has sky-high P/E and P/B ratios. A 115.2x P/E for a SVOD company is a clear sign of overvaluation. Disney’s stock’s P/E ratio is only 16.06x, and its P/B is only 3.55x.

(Source: Finbox.io)

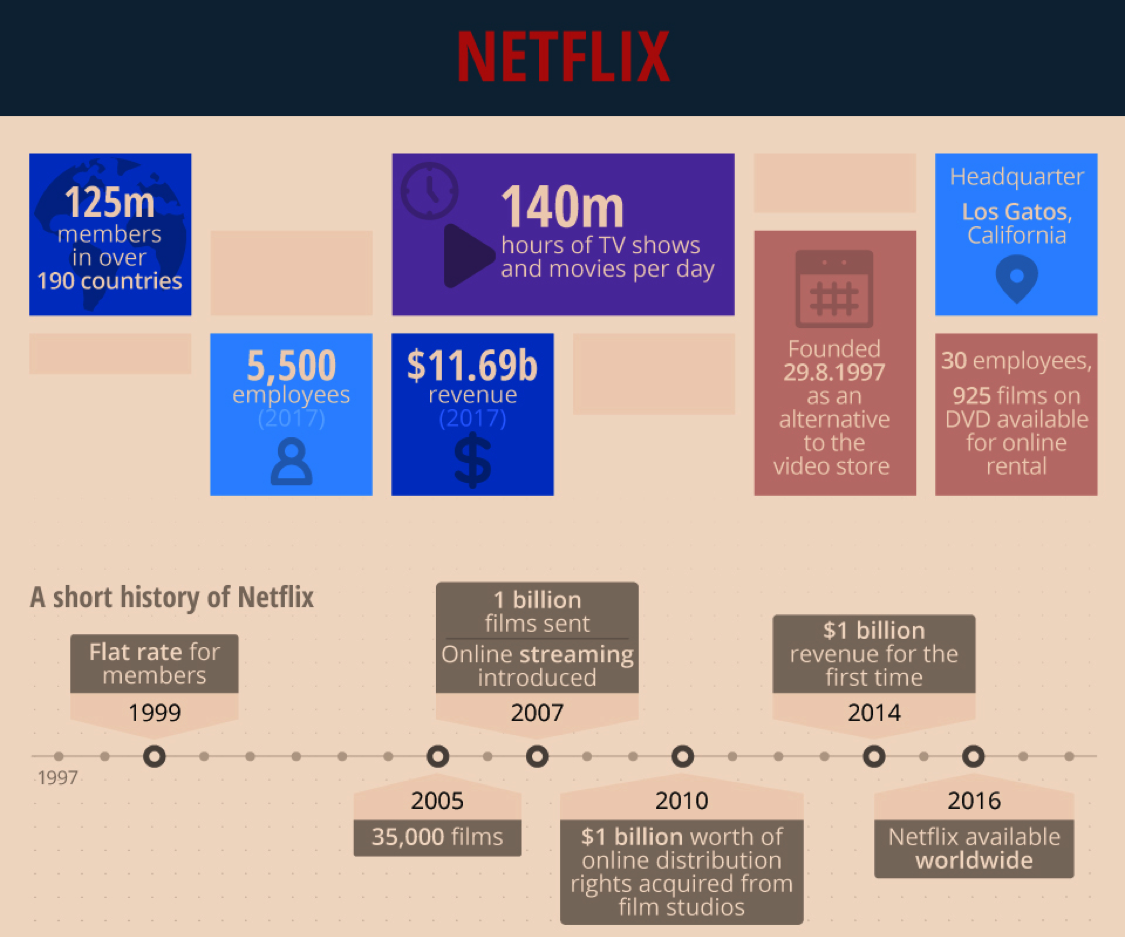

Netflix’s revenue by end of 2017 was only $11.69 billion. It is obviously taking on more debt to finance its aggressive spending on original content. The weak balance sheet is another reason why NFLX has more downside potential. Netflix is now burdened with more than $8.3 billion in debt. Its total liabilities is $18.17 billion.

(Source: finbox.io)

Summary

Low profitability, rising competition, and a large debt load are good reasons why you should avoid investing in Netflix right now. If you have a position, I recommend you sell it now. Netflix is only worth adding to your portfolio after its stock has a more reasonable P/E ratio. Producing better profitability is more important that having more subscribers.

Offering cheap mobile-only subscription plans can lead to a pyrrhic victory for Netflix. There’s little investing attractiveness in a company that has 200 million subscribers and yet producing less than $600 million in annual net profit.

My sell rating on NFLX is also influenced by the following discounted cash flow revenue exit model projection. My fair value guesstimate for Netflix is $236.98.

Past I Know First Successful Forecast Performance

On May 24, 2017 we issued a bullish 1 year forecast for NFLX with a strong bullish signal of 185.88 and with high predictability indicator of 0.39.

Click here to learn how to read the heatmap.

Netflix stock is with a 118.25% return in 1 year. In a good agreement with this bullish forecast.