PepsiCo Stock Price Analysis: Why PepsiCo Should Be In Your Portfolio

The article was written by Motek Moyen Research Seeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

The article was written by Motek Moyen Research Seeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

PepsiCo Stock Analysis

Summary:

- If you like dividend income, PepsiCo should be among your long-term investments. It has a pricey valuation but its diversified sources of revenue are a moat.

- Pepsi has consistently increased its dividend payments for the last 10 years. For the previous 10 years, Pepsi also industriously did share buybacks.

- The management team is also excellent. In spite of declining annual revenue, Pepsi has consistently delivered positive net income for the last 10 years.

- PEP has optimistic medium-term and long-term algorithmic forecasts from I Know First.

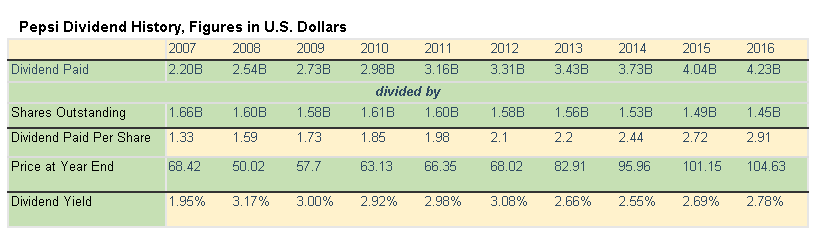

PepsiCo, Inc. (PEP) has rich valuation. PEP has a forward P/E valuation of 20.56. Its Price/Book ratio is also lofty at 13.89x. However, I’m still recommending this stock to people who love dividend income investing. Pepsi is a faithful dividend-giving company for the last 10 years. Pepsi has also consistently delivered annual increases in its dividend payments. Its dividend yield for the last nine years has not fallen below 2.5%.

(Source: Vuru.co/Motek Moyen)

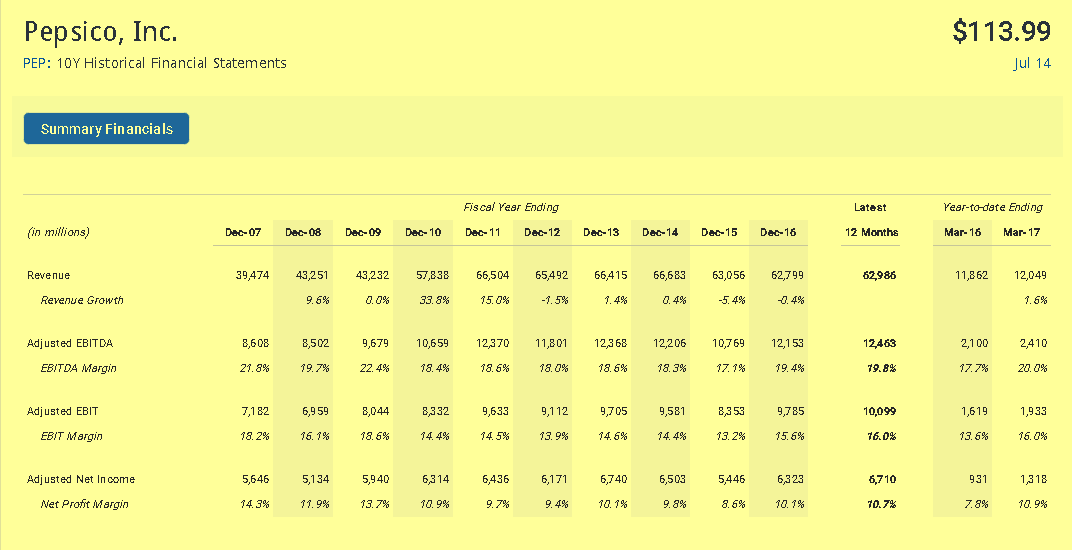

PepsiCo has also been a constant profit generator for the last 10 years. In spite of declining annual revenue, PepsiCo consistently produced positive 9-figure annual net income. Its average net margin for the last decade has been at 10.85%. This consistency is why PepsiCo can afford to keep paying out dividends to its shareholders.

(Source: Motek Moyen/finbox.io)

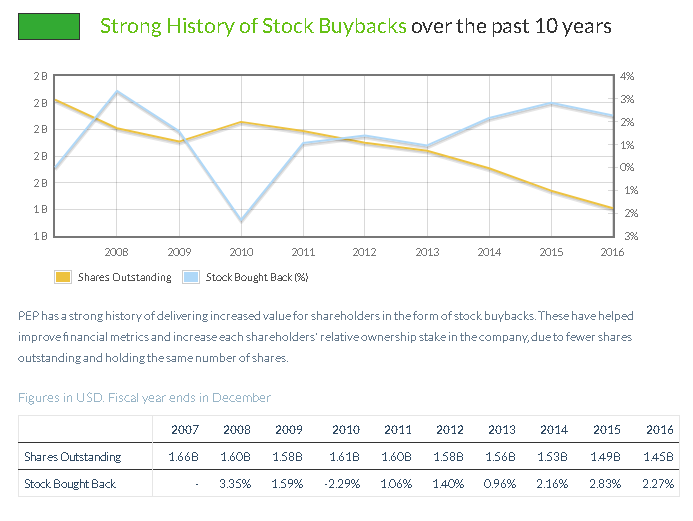

Pepsi’s proven track record of profitability also enablea it to do constant share buybacks. A company actively reducing the number of shares available again benefits shareholders. The persistent habit of stock buybacks helps PepsiCo deliver better financial metrics. The better the financial metrics are, the higher valuation there is for PEP.

Yes, Pepsi has a poor balance sheet. However, as long as the company is profitable enough to do buybacks, it can also easily meet its debt obligations. As of Q1 2017, PEP also has more than $17 billion in cash & equivalents. Pepsi’s free cash flow in Q1 was $1.87 billion.

Yes, Pepsi has a poor balance sheet. However, as long as the company is profitable enough to do buybacks, it can also easily meet its debt obligations. As of Q1 2017, PEP also has more than $17 billion in cash & equivalents. Pepsi’s free cash flow in Q1 was $1.87 billion.

The annual free cash flow of Pepsi for the last three years was $7.3 billion or higher. Pepsi is liquid and has strong cash flow. It is in zero danger of going bankrupt. Pepsi will keep paying its dividends for the next twenty years. This blissful state of Pepsi is why hedge funds are again buying PEP. Institutional and retail investors usually follow where the hedge fund managers are going. For now, hedge fund managers are going long PEP.

(Source: TipRanks)

Well-diversified Business Model

Unlike Coca-Cola (KO), Pepsi has healthy revenue streams outside of its core beverage selling business. Pepsi has 22 billion-dollar consumer brands. Pepsi owns Frito-lay, Quaker, and Tropicana. It also a partner in Lipton and Starbucks (SBUX). Pepsi has put its eggs in many baskets. This company is unlikely to get affected by stricter regulation on sugar level-inducing soft drinks. Pepsi’s operating is largely generated from snacks/food, not from soda drinks.

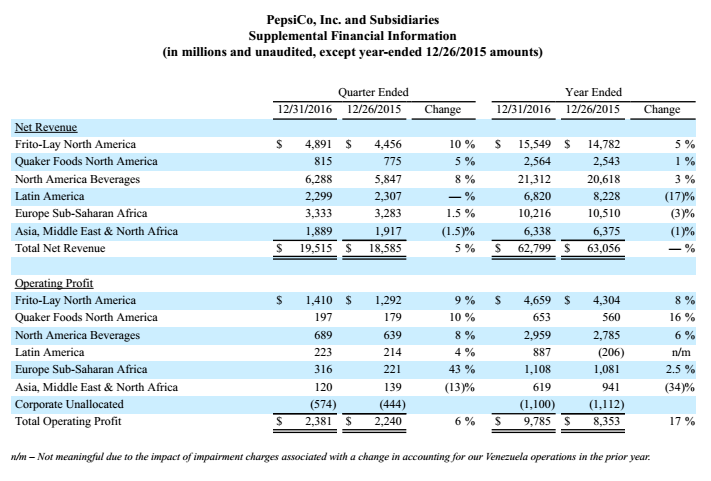

Please study the FY 2016 chart below.

(Source: PepsiCo)

(Source: PepsiCo)

More than half of Pepsi’s $2.38 billion operating profit last year came from its Frito-Lay North America subsidiary. In other words, Pepsi’s profits are coming not from soft drinks/beverages. It comes from its snack brands like Fritos, Doritos, Lay’s, Cheetos, and Munchies.

(Source: Frito-Lays)

(Source: Frito-Lays)

For those health nuts who do not consume salty foods, Pepsi also has Quaker catering to them. Quaker is a global brand giant when it comes to healthy food that diet-conscious people trust. Pepsi is a junk food giant but it also serves products for the fitness-minded individuals. Pepsi also owns AMP, one of the world’s top-selling energy drinks.

Pepsi has also bought Kevita, a probiotics drink manufacturer. It goes to show that Pepsi can also exploit the growing fad for healthy drinks and food. It is adapting to what is in vogue. Expanding beyond its junk food/drinks empire will hopefully reverse the declining revenue of PepsiCo.

Conclusion

Pepsi’s well-diversified product portfolio insures it can keep increasing its dividend payments barring any recession. Dividend income investors should really consider adding PEP to their portfolios. The judicious expansion move of PepsiCO outside it core soft drinks business has helped its stock outperform KO.

In my book, PEP is a better investment than KO right now.

(Source: Google Finance)

My bullish outlook for Pepsi is supported by its positive medium and long-term algorithmic forecasts from I Know First.

My advice is for people to wait for a cheaper entry on Pepsi. PEP’s technical indicators are bearish for the near-term. It is headed for a downtrend. Go long on PEP only when you think it has reached bottom. I’ll go long PEP if it falls below $103.

(Source: StockTA.com)

I Know First Algorithm Heatmap Explanation

The sign of the signal tells in which direction the asset price is expected to go (positive = to go up = Long, negative = to drop = Short position), the signal strength is related to the magnitude of the expected return and is used for ranking purposes of the investment opportunities.

Predictability is the actual fitness function being optimized every day, and can be simplified explained as the correlation based quality measure of the signal. This is a unique indicator of the I Know First algorithm. This allows users to separate and focus on the most predictable assets according to the algorithm. Ranging between -1 and 1, one should focus on predictability levels significantly above 0 in order to fill confident about/trust the signal.