Quantitative Trading: Quantitative AI Equity Funds Rebirth

The article was written by Dmitry Podretskiy, a Financial Analyst at I Know First.

Quantitative Trading: Quantitative AI Equity Funds Rebirth

Summary

- AI transforms investment strategies

- Pre-crisis market overview

- Quantitative strategies meltdown

- Goldman’s QIS renaissance

- I Know First implementing AI

More than half of Americans invest in the stocks through mutual funds, direct share ownership, etc. For households with income greater than $70,000, this proportion jumps to 85%. Many of these investors rely on professionals like financial advisers or brokers to choose an investment strategy. These professionals are referring to AI more and more nowadays for assistance.

Almost 1.5 thousand funds rely on computer modelling to trade stocks and other investments. Most of them are traditional quantitative funds. But the growing number of hedge funds are guided by AI-powered trading engines. And as some markets been already transformed by AI, these engines show absolute new investment ways and products, while raising new questions.

In a recent article, wired.com said, “The machines, however, are getting smarter. Each day, after analyzing everything from market prices and volumes to macroeconomic data and corporate accounting documents, these AI engines make their market predictions and then “vote” on the best course of action.”

To better understand the different players, Etienne Brunet from Illuminate Financial published the map where he categorized the various players in the market. Below is a landscape mapping with major companies.

Source: Etienne Brunet

Quantitative Funds Meltdown

The year 2007 was a peak for quantitative funds development with a promising and expanding industry. Until a colossal failure in quantitative equity funds worldwide shook the whole base.

On August 6, 2007, as soon as US markets started trading, previously wildly successful automated investment algorithms coded by the Goldman’s Quantitative Investment Strategies team (QIS) went horribly wrong and losses mounted at a frightening pace. During the week of August 6, a number of quantitative long/short equity hedge funds experienced unprecedented losses.

“All this worked academically, and for a long time it worked in practice, and then all of a sudden you have this horrible event,” Mr. Chropuvka says (one of two partners leading the QIS team at Goldman in New York). “It was the most humbling experience of our lives.”

Chain Reaction

Such “quant” funds were popular among hedge-fund investors. Many use a market-neutral strategy, which aims to balance long positions with short trades, or bets against securities. Others are so-called statistical arbitrage funds, which analyze the historical relationships between relating securities and trade when those relationships get out of blow.

A lot of players in this part of the hedge-fund business have similar positions and use lots of leverage, or borrowed money, to increase their bets. However, that boosts even small losses. Some of these hedge funds also have relatively permissive redemption periods, allowing investors to take their money out every month, with 30 days’ notice or less.

So if losses lead to investor redemptions, these funds may have to sell lots of their positions. That, in turn, puts more pressure on the historical relationship between related securities, handing more losses to other hedge funds during this time.

If such positions are sold by lots of managers at the same time, the most leveraged funds get hit the hardest, possibly forcing big liquidations of portfolios, which cause a chain reaction.

Goldman Sachs and JPMorgan losses during Aug. 11, 2007, after quant quake

Combo Effects

Using transactions data, it was discovered that the simulated returns of a simple market-making strategy were significantly negative during the week of August 6, 2007, but positive before and after. It said, that the “Quant Meltdown” of August was the combining effects of portfolio deleveraging throughout July and the first week of August, and a temporary withdrawal of market-making risk capital starting August 8th.

These conclusions have significant implications for the systemic risks posed by the hedge-fund industry.

Even Renaissance Technologies, the well-known hedge fund co-founded by cold war codebreaker James Simons, suffered painful losses, and it nearly obliterated Goldman’s QIS.

But Goldman wasn’t the only hedge-fund giant to be hit by such problems. A lot of other big firms that specialize in quant strategies also suffered losses. Including Jim Simons’ Renaissance Capital, Clifford Asness’ AQR Capital Management and Tykhe Capital LLC, run by former D.E. Shaw traders.

Quant Renaissance

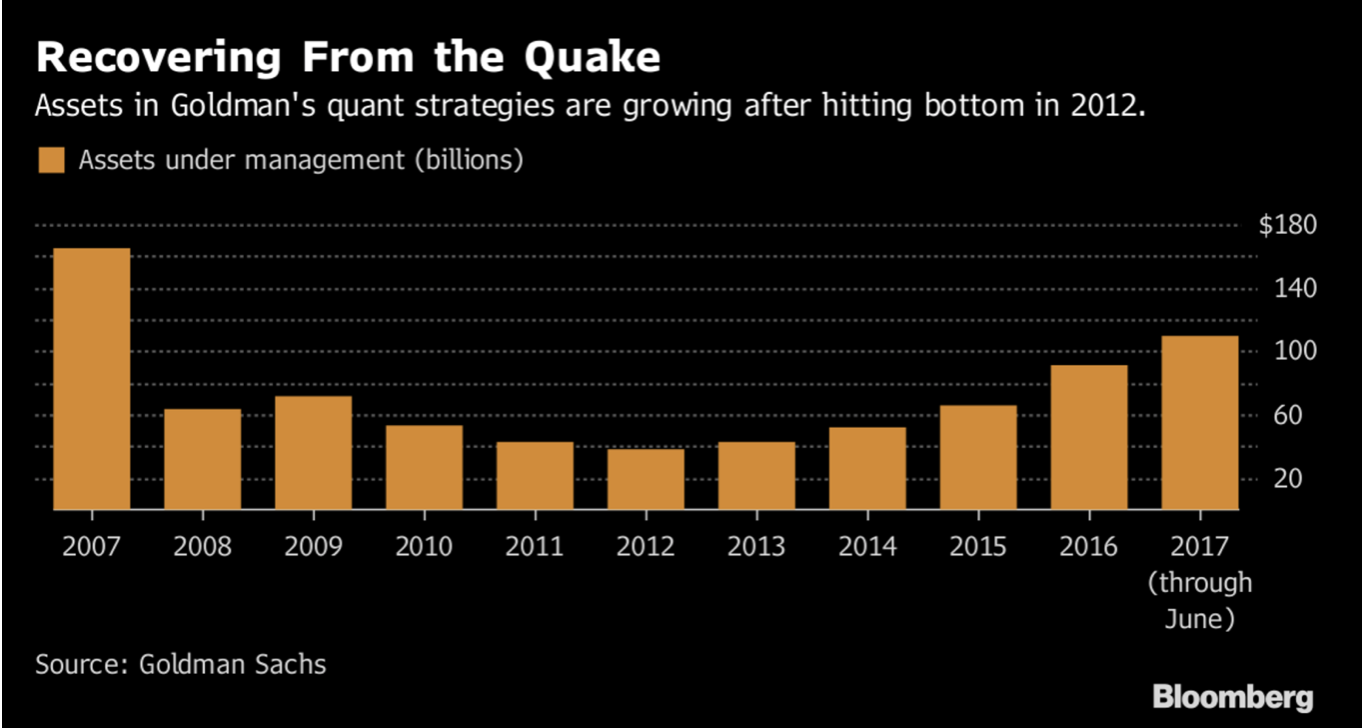

Nearly a decade later, nowadays quantitative investing is once again the hottest trend in finance. Computer-driven hedge funds have just doubled their assets from 2009 to $918bn, according to Hedge Fund Research.

QIS is etalon of the quant renaissance. In 2012 assets under management reached a bottom line of $38bn. Now it manages $91.8bn — still below the unit’s pre-crisis peak.

The huge growth of algorithmic investing has transformed the markets. Some analysts fear that another 2007-style meltdown would be more severe due to the spreading of quant strategies. The growth of quant hedge funds is like a decade ago. They are everywhere in the investment world. In 2007 the problem was localized, but now everyone uses the same strategies. Quant strategies now have about 14% of all hedge fund assets, as in 2007 it was 8%.

QIS was totally rebuilt for the decade since its near death. The team had been focused on three main areas: tax-efficient strategies; “smart beta” business, which invests in specific market factors; and “equity alpha”.

The future of business will be powered by big data. QIS is consuming data for its almost 15,000 stocks from more than million locations. It uses “machine learning” to find and qualify links and relations between companies. QIS has about $110 billion in big data mutual funds and other instruments, mostly driven by behavioral consumer’s factors.

The QIS use leverage today only for few offerings and looking through markets to detect signals of overcrowding. “Smart beta” is the biggest part of today’s Goldman quant unit with $77 billion in investments. Beta is tracking indexes on points such as low valuation and momentum. In a number of U.S. mutual funds QIS also use big data strategies.

Overcrowding

Sometimes signals can stop working, recommendations changes. What used to be an indicator is changing because it’s losing predictive power. And more important, quantitative funds have produced quite a scanty return of 0.1% – 2%.

Bridgewater’s “Pure Alpha” made only 2.4% in 2016. London-based Winton Group shows 1.47% this year after losing 3% last year. The $4 billion Man Group also fell 3% last year and trying to return only 2% now, etc.

Despite alarming factors, there is a great demand for quantum strategies. Deutsche bank survey, released in March 2017, is mirroring situation: “The number of available strategies has been growing and now range from simple low fee alternative risk products to more complex high alpha products that have seen further enhancements due to the advances in areas such as machine learning, quantum computing and the cloud. This has contributed to the additional interest and demand”.

According to the survey hedge funds expected to perform in 2017, driving industry growth. Close to three-quarters of investors expect their hedge fund portfolios to perform better in 2017 vs 2016. Performance-based gains driving industry assets to reach more than 3 trillion US dollars by end of the year. It follows same studies by Goldman Sachs and Barclays in 2016: 20 percent of investors were interested in quant strategies.

But some analysts sounds alarming. Too much money following the same strategy already led to problems. Bloomberg, according to a Bank of America quant strategy report: “Good quantitative signals perform well in the short term, but the decay rate is extreme. New signals tend to be exploited and then quickly utilized away”.

Jonathon Jacobson, the founder of Highfields Capital Management, questioned the sustainability of quant performance in a second-quarter letter to investors. “Hundreds of billions of dollars can’t exploit the same inefficiency for long,” the hedge fund manager wrote. “My sense is we are a lot closer to the end than the beginning of these strategies producing excess returns.”

I Know First’s Implementation of Artificial Intelligence Technology

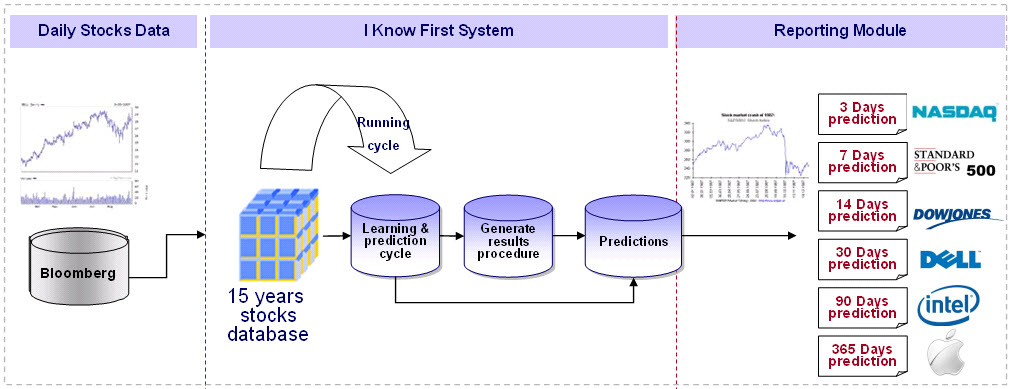

I Know First predicts a growing universe of over 10,000 securities for the short, medium and long term horizons daily by applying Artificial Intelligence and Machine Learning techniques to search for patterns and relationships in large sets of historical stock market data.

I Know First is among 5 start-ups, who showcased their solutions in Payments, Finance Management, Security and other specialties according to Israel Economic Mission in the USA.

Through its self-learning ability and flexible multi-layered neural networks structure, the algorithm is able to learn from, adapt to and evolve together with continuously changing markets. It offers an independent, objective and unique perspective on the financial markets and doesn’t rely on any human derived assumptions or traditional theories and models that often do not hold (anymore).

The results of intense learning and prediction cycles are aggregated into two indicators per time frame: signal and predictability. While predictability indicator helps to identify and focus on the most predictable assets, the signal is used to define and rank the trades and is related to the magnitude of expected return.

The applications of the algorithmic AI-based forecasts are multi-fold.

The scalability of the algorithmic predictive system allows I Know First to offer custom forecasting solutions to hedge funds and other financial institutions, so they can identify the best opportunities as discovered by the self-learning algorithm within the investment universe of their interest. Further, the solution can be used as a decision support system in form of an algorithmic screen integrated into client’s investment process in order to confirm or reject investment ideas before the execution.

Moreover, I Know First develops and back-tests systematic trading strategies which are used in partnerships with hedge funds and other asset managing entities. These strategies are rules-based and utilize algorithmic forecasting indicators mentioned above in order to rank and select the trades as well as the time the execution. The type of strategies varies, including mean-reversion logic and more trend focused approaches, all generating high positive alpha while keeping beta in the 0.3-0.8 range, yielding overall high risk-adjusted returns. The strategies can be used in partnership with I Know First to launch hedge funds, mutual funds or other investment vehicles.