QCOM Stock Analysis: Qualcomm And Apple Will Likely Settle Their Patents Licensing Dispute

The article was written by Motek Moyen Research Seeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

The article was written by Motek Moyen Research Seeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

QCOM Stock Analysis

Summary:

- Apple sued Qualcomm last January for allegedly overcharging on patent licensing fees. Apple also stopped paying royalty fees to Qualcomm earlier this year.

- In retaliation, Qualcomm sued in May four contract manufacturer partners of Apple, Foxconn, Compal, Pegatron, and Wistron. Qualcomm has also sued Apple in the U.S. federal court and the ITC.

- The ITC or the U.S. International Trade Commission announced last August 8 that it will proceed with the patent infringement suit filed by Qualcomm against Apple.

- Apple settled its patent dispute with Nokia. Nokia filed suit earlier this year aiming to ban sales of iPhones in key countries. Apple made an upfront payment of $2 billion to settle with Nokia.

- I expect Apple to also settle out of court with Qualcomm before 2017 ends. It is always cheaper to pay patents licensing fees than risk a court-ordered import ban on iPhones.

Nokia (NOK) got an upfront payment of $2 billion from Apple as an out-of-court settlement over their patent licensing dispute. In line with this development, I also expect Apple to capitulate soon on its patent licensing court drama against Qualcomm (QCOM). Beyond all the indignation and mighty chest-pounding from Apple, it really has a weak chance of proving its iPhone products don’t violate the numerous patents of Qualcomm.

Apple already lost multiple times against the patent infringement suit filed by the Wisconsin Alumni Research Foundation. It doesn’t need another humiliation at the court against Qualcomm. The patent infringement suit filed by Qualcomm against Apple last July covered six new patents. They are not yet covered by existing licensing contracts with Apple and/or its manufacturing partners. They are new legalized bullets that Apple is unlikely to dodge by arguing that Qualcomm was overcharging it on their existing patent licensing agreement.

(Source: Qualcomm)

(Source: Qualcomm)

The U.S. International Trade Commission (ITC) found merit and already decided to investigate Qualcomm’s patent infringement suit against Apple. Qualcomm’s case alleges Apple committed violations of section 337 of the Tariff Act of 1930 in the importation of electronics devices that reportedly are infringing on patents owned by Qualcomm. Meaning, the ITC will decide if it should ban the importation/sales of iPhones and iPads to the United States.

Why Apple Will Settle Soon

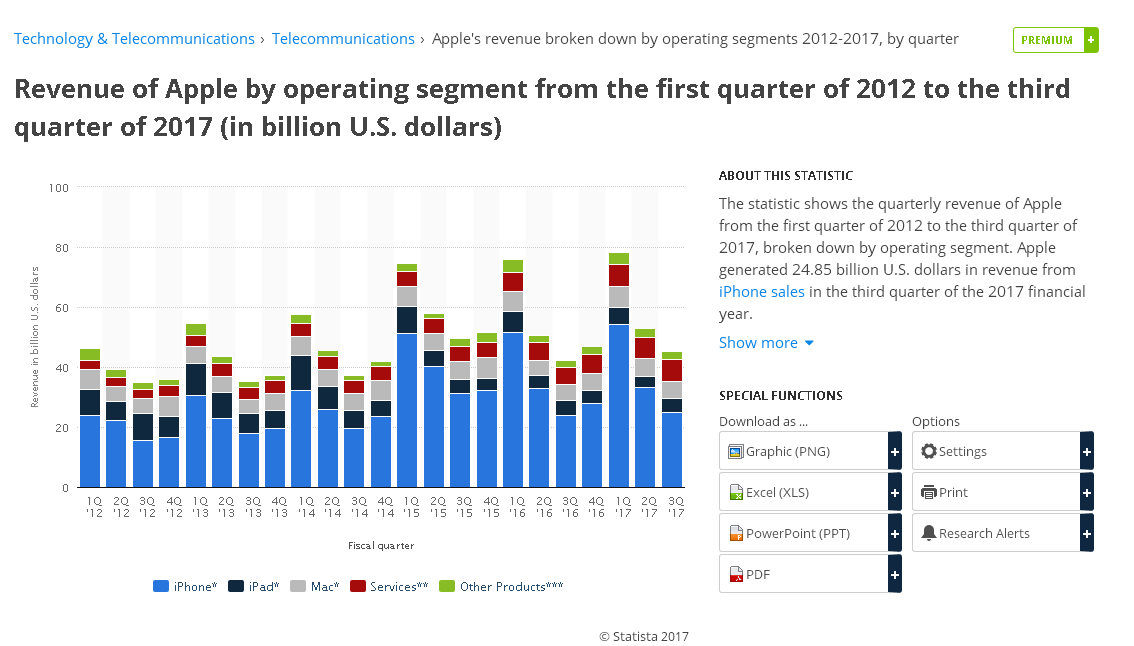

Apple iPhone and iPad products are manufactured in China. They are vulnerable to court-ordered import bans. An out of court settlement deal is likely to happen soon. Apple will be in trouble if the ITC decides in favor of Qualcomm’s request to ban iPhone 7 importation in the United States. Apple generates 70% of its revenue from iPhone sales. A import ban in the U.S. is really going to hurt Apple’s iPhone sales.

Qualcomm has the upper hand when its patent infringement suit threatens the iPhone sales of Apple.

(Source: Statista)

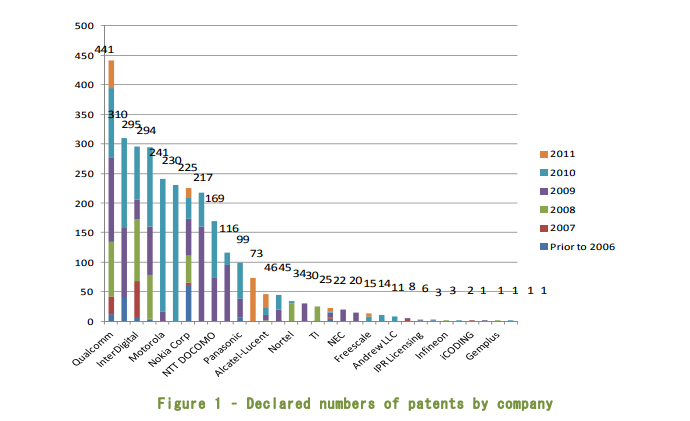

It will be cheaper to play nice with Qualcomm and settle the case out of court. Apple, faced by Nokia’s patent infringement suits threatening import bans against iPhones, had to cave in and pay what Nokia wanted. Aside from the six new patents on which Qualcomm is suing Apple, Qualcomm really touts the most number of Standard Essential Patents covering LTE/4G connectivity. Qualcomm has 441 patents, Nokia only has 241.

(Source: cybersoken)

Apple wants to pay licensing/royalty fees on patents involving baseband/connectivity parts of the iPhone. Qualcomm apparently wants to charge based on the retail price of the whole iPhone. Qualcomm could accommodate a fee based on a discounted value of the iPhone and Apple will likely settle.

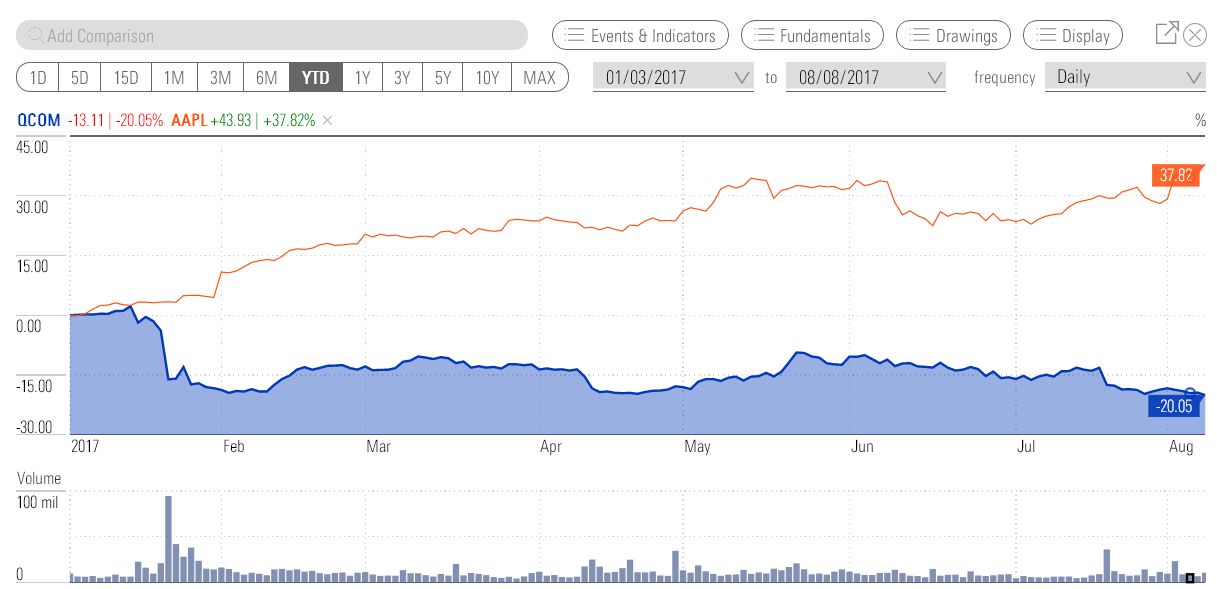

Qualcomm only needs to be humble and it should start the negotiation for an out of court settlement. Apple’s management will try to save face and it will please them if Qualcomm makes the first move to settle the row. Qualcomm being friends again with Apple will most likely improve QCOM’s poor performance this year, -20% YTD.

(Source: Morningstar)

The negative YTD performance of QCOM is partly due to Apple’s refusal to pay royalty fees owed to Qualcomm. It is to the welfare of Qualcomm to get Apple paying patent licensing and royalty fees again.

Conclusion

An out of court settlement from Apple could boost QCOM’s price by 10% or more. I therefore rate QCOM as a buy. It is Apple’s Achilles Heel that it doesn’t have a strong library of patents. Its success in smartphones is always reliant on other companies’ patents and IP assets. Going forward, Qualcomm will continue to enjoy healthy patent licensing and royalty fees from smartphone vendors like Apple.

Further, the depressed price of QCOM has made its dividend yield higher than 4%. It is now therefore a bargain buy for income-minded investors. Qualcomm touts a very strong history of paying dividends over the last decade. I believe its huge library of patents will help it repeat this feat for the next decade. Everybody have to pay Qualcomm’s patent toll booth before they can pass on to greater success.

(Source: vuru.co)

I Know First has a bullish one-year algorithmic market trend forecast for QCOM. We should keep the faith that QCOM will eventually trade above $60 again.

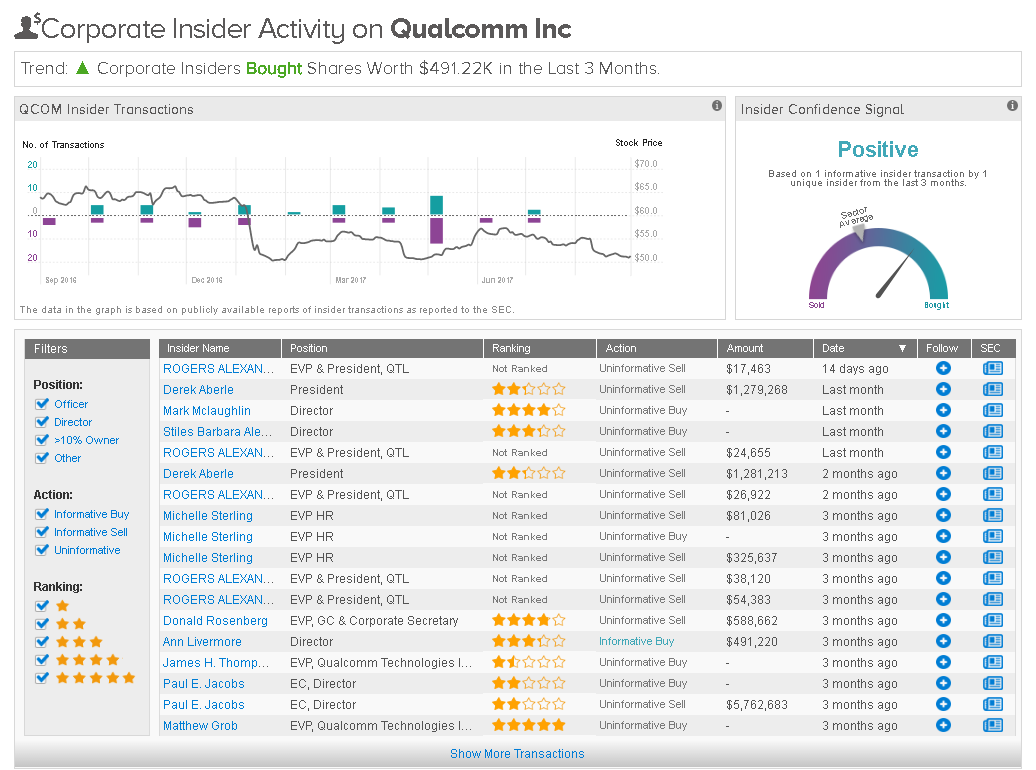

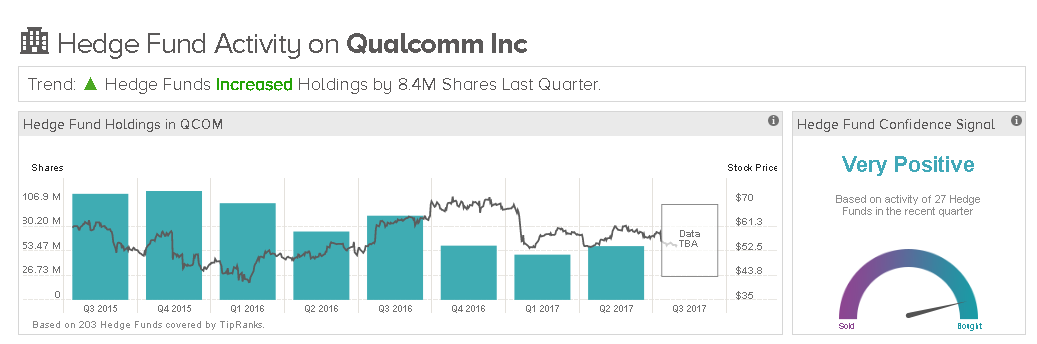

My bullish outlook for QCOM is also backed by the positive confidence signals from hedge fund managers and from Qualcomm insiders. Insiders are not dumping QCOM, and hedge fund managers are going long QCOM. The average 12-month price target of TipRanks-tracked analysts for Qualcomm is $61.89.

(Source: Motek Moyen’s TipRanks account)

(Source: Motek Moyen’s TipRanks account)

I Know First Algorithm Heatmap Explanation

The sign of the signal tells in which direction the asset price is expected to go (positive = to go up = Long, negative = to drop = Short position), the signal strength is related to the magnitude of the expected return and is used for ranking purposes of the investment opportunities.

Predictability is the actual fitness function being optimized every day, and can be simplified explained as the correlation based quality measure of the signal. This is a unique indicator of the I Know First algorithm. This allows users to separate and focus on the most predictable assets according to the algorithm. Ranging between -1 and 1, one should focus on predictability levels significantly above 0 in order to fill confident about/trust the signal.