MU Stock Prediction: Going Long With Micron

This article was written by the I Know First Research Team.

This article was written by the I Know First Research Team.Summary:

- Cautious buy rating for short to medium term but bullish in the long run for MU Stock

- Oversupply of chips is still in recovery, declining prices are not alarming

- Trade war and ban on Huawei is unlikely to last for long

- Unlikely that China’s local DRAM chip, Changxin Memory Technologies, will replace Micron

Micron Technology (MU) is the third largest supplier of semiconductor chips, NAND and DRAM, in the world. Their shares plunged 22.5% in the month of May.

MU stock is facing troubles from inventory buildup, trade wars, ban on Huawei and China’s own locally produced chip. With China accounting for over half of Micron’s sales, the company is facing significant headwinds.

However, we can remain hopeful that Micron’s stock prices will recover in the long run.

My stance is that we remain bullish on Micron in the long term. But be cautious on the short to medium to term. This article will aim to convince you on why you should remain bullish on Micron despite all the recent setbacks.

MU Stock Prices Decline But Do Not Be Alarmed

Many semiconductor firms including Micron are still suffering from the impact of the oversupply of DRAM and NAND chips. The demand for smartphones were overwhelmingly low last year.

Now, Micron’s customers are still working through their inventories before they will start to purchase more chips again.

During fiscal Q2 Micron grew revenues and expanded gross margins year over year. This was despite adverse memory and storage pricing and weakness in smartphone unit sales. Additionally, NAND bit shipments grew more than 5 times year over year.

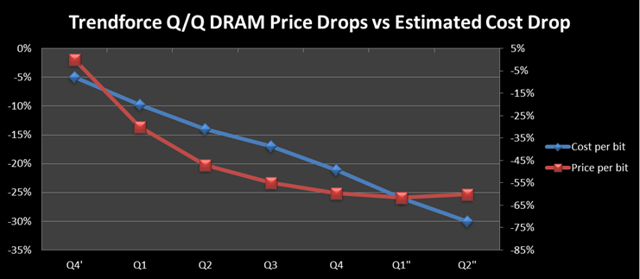

One might think that a decline in DRAM prices would mean that there is no recovery in the DRAM market. However, DRAM prices can decline and be in recovery simultaneously.

When the pricing does not drop as fast as the cost of a bit, it allows cost improvements to catch up and be profitable. With slower pricing drops each quarter, the cost per bit will eventually be lower.

Hence, even though DRAM prices are still in decline, I would not be too concerned about it.

Trade War & Ban On Huawei Will Not Be Here To Stay

China produced 57% of Micron’s sales in 2018 and its dependency on China is not something to be overlooked. Micron sits in a very precarious situation and is heavily impacted by the decisions of the Trump administration.

However, it is very difficult for China to be completely self sufficient in their production of semiconductor chips. A compromise between the US and China has to be reached sooner or later.

13% of Micron’s total revenue came from Huawei in the first half of 2019. Micron suspended its shipments of chips to Huawei in late May. This was a response to the Trump administration’s decision to blacklist the tech giant from US technologies.

Huawei is the third largest phone smartphone manufacturer in the world, behind Apple and Samsung. The sale of chips to Huawei brings Micron a huge market share in the smartphone market.

China’s Own DRAM Chip – Nothing To Worry About In The Long Run

Not to mention, China recently showcased their first domestically designed DRAM chip. Changxin Memory Technologies and has already invested $8 billion into its DRAM operations. It has also allocated up to $1.5 billion in CapEx for the current year.

As compared to Micron, which has a CapEx forecast up to $9 billion this year, it is a small amount. However, it is more than twice the amount of the fourth largest DRAM maker in the world, Nanya Technology.

China is looking to push foreign chip makers out of the market and flood the market with local chips. Chinese authorities launched antitrust probes against Micron, Samsung, and SK Hynix.

However, all this news from mainland media could just be to boost nationalistic pride. Chances that Huawei can prosper with the US ban and without Micron is slim to none.

The truth is that China’s tech companies are heavily reliant on US components and they cannot easily be replaced. Even substituting with Korean and Japanese suppliers would be subject to penalties as they rely on US intellectual property.

Source: Reuters

“China cannot succeed if it is entirely dependent on indigenous innovation.”

Founder of Huawei, Ren Zhengfe

China’s past attempts to design and fabricate its own chips have also come up short.

For example, 12 years after it was set up to produce NAND memory chips, Yangtze Memory Technologies still remains five years behind Samsung. And following theft allegations of intellectual properties from Micron, Fujian Jinhua Integrated Circuit collapsed after US export controls.

MU’s track record proves itself

Despite its recent setbacks, Micron is a strong competitor. It has a track record of beating analysts’ revenue and earnings estimates. The upcoming quarter results on 25 June 2019. I believe it will beat analysts estimates yet again.

Furthermore, Micron has a history of executing their strategy well. They focus on improving cost competitiveness and increasing high-value solutions.

This strategy has improved Micron’s annualized profitability by over $6 billion from fiscal 2016 to fiscal 2018. This has also improved its EBITDA margin by more than 15% relative to their competitors.

Micron is well-accomplished in using revenue to generate returns. It has a Return on Total Capital of 43.60 and Return on Invested Capital of 38.60%. Its Return on Equity is 55.52, and Return on Assets is 35.92.

Conclusion

To conclude, I believe that Micron will be able to make a strong recovery in the long run. However, I would give it a cautious buy rating for the medium to short term.

Despite declining prices of DRAM chips, slower price drops per quarter will still allow it to be profitable.

Also, the Chinese economy cannot prosper if they pursue technological self sufficiency. I believe that the US and China’s government will come to an agreement that will work in Micron’s favour in the future.

Additionally, I expect Micron’s chip sales to improve in 2020. The onset of the latest technologies will drive phone sales. 5G, foldable phones and upcoming innovations in augmented and virtual reality will make use of Micron’s chips.

Current I Know First MU Stock Prediction

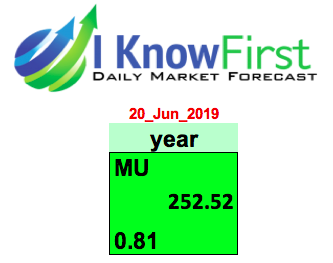

The I Know First machine learning algorithm currently has a positive outlook for MU. The stock is bullish over a year horizon. It has a signal of 252.52 and predictability indicator of 0.81.

I Know First Algorithm Past Success with MU Stock

On 6 January 2019, I Know First algorithm made a bullish forecast on MU stock. The time frame was 3 months. From 6 January 2019 to 6 April 2019, MU grew by 31.19%, confirming I Know First’s forecast.

This bullish MU stock forecast was sent to the current I Know First subscribers on 6 January 2019.

To subscribe today click here.

Please note-for trading decisions use the most recent forecast.