Cleveland-Cliffs Stock Forecast: Cleveland-Cliffs (NYSE: CLF) is Back to Basics

This article was written by Isabelle Tao, a Financial Analyst at I Know First.

CLF Stock Forecast

“Cleveland-Cliffs was founded and was very successful doing one thing and one thing only, and that was serving the steel industry in the United States with high-quality, customized iron units” – Lourenco Goncalves, CEO

Summary

Cleveland-Cliffs focused the business back to the iron ore industry in North America

High demand for Electric Arc Furnace (EAF) is driving growth

With Chinese metals dwindling in the United States after Section 232 is implemented, CLF will only grow more

Currently, I Know First algorithm forecast is bullish for CLF in the long-term

CLF deserves to be congratulated. On July 20th, CLF released their Q2 Results with an adjusted EBITDA of $276 million, which was more than double the EBITDA performance in the year-ago quarter. The earnings call claimed it was the best quarterly result since 2014. Net income increased by 370.52% from the previous quarter and EPS was at $0.55/share, higher than the estimated $0.52/share.

(Source: Flickr)

(Source: Flickr)

Cleveland-Cliffs Inc, formerly Cliffs Natural Resources Inc., with a corporate heritage dating back 170 years, is the largest supplier of iron ore pellets to the North American steel industry. It is also one of the lowest cost producers in the world. The Company sells in mainly two segments: US Iron Ore and Asia Pacific Iron Ore, with mines in Michigan, Minnesota and Western Australia.

Growth in recent months

2017 has been the most successful year for Cliffs since 2014. Gone were the days when the company almost went bankrupt as iron ore prices dropped to multi-year lows in 2015. CEO Goncalves said since he took over, “the biggest accomplishment was avoiding bankruptcy”. Now, the market can no longer ignore its bigger accomplishments.

Apart from doubling its EBITDA last quarter, Cliffs has done well from an annual point of view. Total sales increased by 9.69% and net income also grew by 31.63%. At the meantime, EPS increased by 45.38% year on year. The main reason for this growth was the strength of the domestic steel market, which led to a higher demand for pellets and higher prices customers pay for pellets. The company sold 6 million long tons in Q2 2018 at a price of $112.6 per ton, and increased its projected sales to 21 million tons in the next year. Sales were up 38% from the 4.3 million long tons in the year-ago quarter.

CLF Management or Steel Tariffs?

We ran an article in the past analyzing how the Trump administration tariffs would help Cliff. Two years on, it is vital to ask whether the growth was due to the trade tariffs (Section 232) or a growing American steel economy. While it is easy to assume that trade tariffs “saved” the American metal economy, it is crucial to note that most tariffs have yet to materialize. Most of Cliff’s 2017 earnings were based on their 2016 contracts. In a CNBC interview, CEO Lourenco Goncalves explained that their earnings are due to higher demand and a strong economy. Hence, with the Section 232 tariffs coming into effect, I would expect the stock to grow even more in the future.

CLF also has an interesting take on China. As with other commodity markets, CLF could not compete against China’s “absurdly low wages, lack of pollution control (that creates unacceptable production shortcuts) and government subsidies to overproduce (that crashes other country’s markets)”. However, from another perspective, China has an increasing need to import high-quality iron ore. China is currently transiting from extremely polluting production to more environmentally-friendly production. One way to achieve this is by using Electric Arc Furnace (EAF) which require high-quality iron ore and scrap metal. However, high-quality iron ore needs a lot of water and is not present in competitor plants in West Australia. Hence, China would eventually import scraps from the US, which increases prices and pushes high-quality iron ore demand up. Instead of seeing China as a competitor, it sees China as an opportunity.

“Back to Basics” strategy and why diversification failed

The “back-to-basics” strategy is one introduced by CEO Lourenco Goncalves. It returned the 170-year old company to its roots in North America. Before, the company held Canadian assets, coal assets, chromite assets and nickel assets. However, transportation and management cost across such a diverse portfolio only distracted CLF and piled up its debts.

(Source: Wikimedia Commons)

After selling off many of these peripheral assets and focusing on North America, the company solidified its outstanding supply chain, reduced transportation costs and went back to what it does best: producing and selling iron ore pellets in the United States. “Annualized interest expense, which at one point hovered around $230 million, has been reduced to just $96 million per year,” Tim Flanagan, CFO, told analysts in Cliffs’ 2017 third-quarter earnings conference call.

New HBI plant and how it fuels growth

Steelmakers shifted from all integrated or blast-furnace-based to vast-majority EAFs in the past 30 years. Hence, CLF is repositioning itself to be the main supplier of EAF that has dramatically reordered the North American steel production base.

Electric Arc Furnace

(Source: Wikimedia Commons)

Cliffs announced plans in June 2017 to construct a $700 million, hot-briquetted iron (HBI) plant in Toledo, Ohio, to serve the EAF-based steel market in the Great Lakes region. This plant will generate 1200 jobs. At the time of the announcement, Cliffs expected to break ground on the facility, which will be capable of producing 1.6 million metric tons of HBI annually, early this year. HBI is not a replacement for steel scraps, but an upgrade because it could be controlled and customized based on what the consumers want. How has the HBI project been proceeding and has it experienced cost pressures? According to Cliffs, it is comfortable with the cost and margins of building the HBI so far.

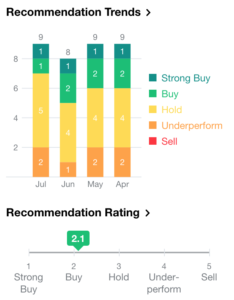

Analyst Recommendations

(Source: Yahoo Finance)

The current analyst consensus rating supposed at 2.1 on company shares (1.0 Strong Buy, 2.0 Buy, 3.0 Hold, 4.0 Sell, 5.0 Strong Sell).

Conclusive thoughts

The company went almost under in 2015 when iron ore prices dropped to an all-time low. One of the reasons why it got back up was the CEO, Lourenco Goncalves who massively cut costs and restructured the company. The ability to push through a crisis and walk the fine line between refocusing the company and managing the financial issues shows resilience and capability. With a stable and high demand, I confirm the buy recommendation for CLF. That resonates with current bullish I Know First forecast.

Current I Know First Bullish Forecast

My recommendation is supported by the forecast of I Know First. On June 15th, 2018, I Know First issued a bullish forecast for CLF with the one month signal of 38.80 and predictability of 0.54. The long-term signal is even stronger at 328.45 in one-year forecast.

How to read the I Know First Forecast and Heatmap

Past I Know First Success with CLF

On April 4, 2016, the I Know First self-learning algorithm showed a bullish outlook on CLF over a 1 year period with a signal of 685.81 and predictability of 0.81 as part of the dividends package. In accordance with this prediction, CLF increased by 177.26% over this time period, highlighting the I Know First algorithm’s success with predicting CLF’s stock in the past.

Current I Know First subscribers received this bullish CLF forecast on April 3rd, 2016.

Please note-for trading decisions use the most recent forecast.

Get today’s forecast and Top stock picks.