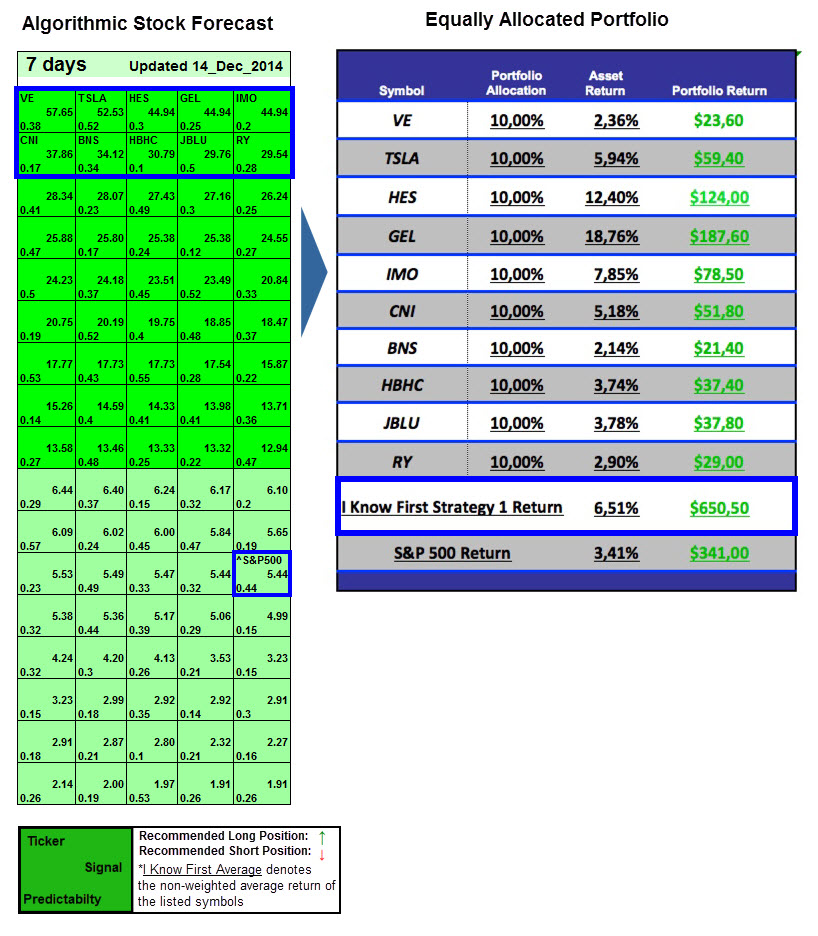

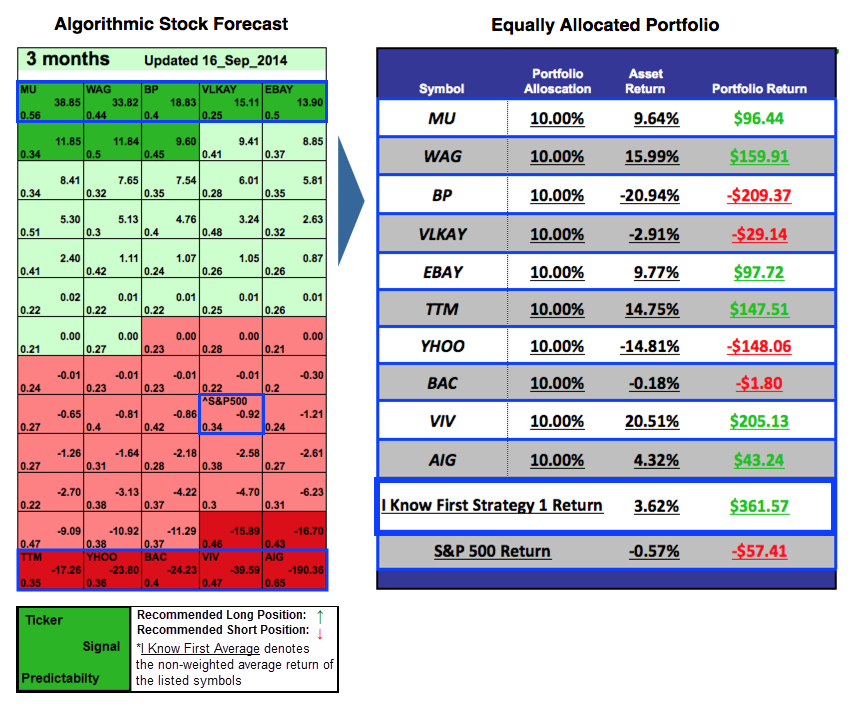

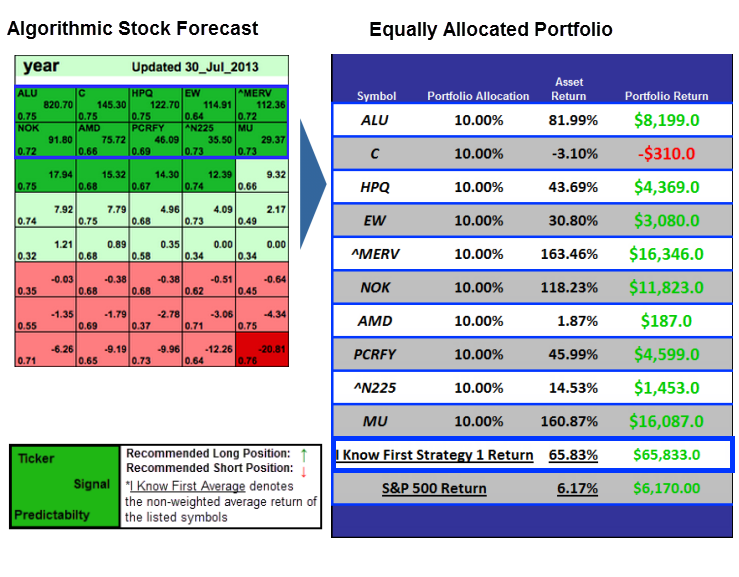

I Know First Algorithmic Trading Strategies: Complete Overview There are multiple algorithmic trading strategies investors can apply when using I Know First’s self-learning algorithm as seen here. After fully understanding how to interpret the heat map, you can construct your own personal portfolio to further optimize returns.

I Know First Algorithmic Trading Strategies: Complete Overview There are multiple algorithmic trading strategies investors can apply when using I Know First’s self-learning algorithm as seen here. After fully understanding how to interpret the heat map, you can construct your own personal portfolio to further optimize returns.

I Know First Algorithmic Trading Strategies: July 30th 2014 There are multiple strategies investors can apply when using I Know First’s self-learning algorithm as seen here. After fully understanding how to interpret the heat map, you can construct your own personal portfolio to further optimize returns. Click Here For Full Story

I Know First Algorithmic Trading Strategies: Complete Overview

There are multiple algorithmic trading strategies investors can apply when using I Know First’s self-learning algorithm as seen here. After fully understanding how to interpret the heat map, you can construct your own personal portfolio to further optimize returns.

Google (NASDAQ:GOOG) (NASDAQ:GOOGL) reported a fantastic second quarter and Wall Street reciprocated with shares jumping in the following days. Results surged way beyond last year's second quarter report and the company successfully beat most analysts' revenue expectations. As this jump in value is certainly justified, there are still some concerns that we should not forget including Google's declining cost-per-click, and the Facebook's (NASDAQ:FB) growing share of the mobile advertising market. On the other hand, Google has future prospects that should have investors excited about the company's future. From utilizing YouTube ads to pushing the innovation envelope with Google Glass, the long-term prospects are certainly interesting and if executed correctly, shareholders will be rewarded.

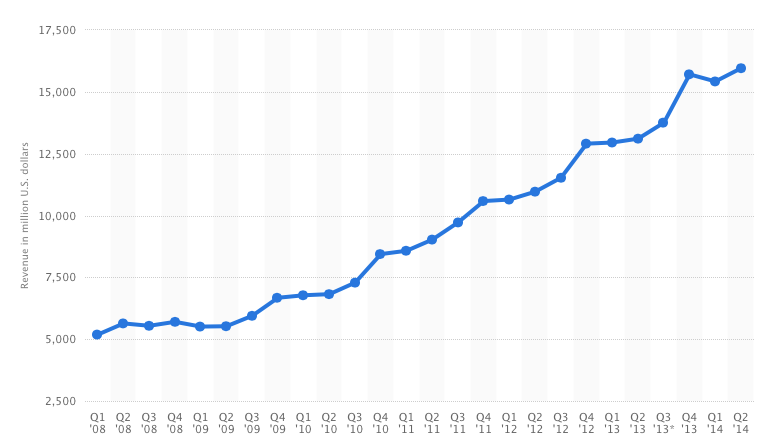

The company's performance this past quarter was impressive on most figures including increased revenue that was up 22%, from $12.67 billion in the second quarter of 2013 to $15.96 billion in 2Q14. Google's Non-GAAP net income came in at $4.18 billion in the second quarter, beating $3.36 billion in the same quarter last year. "Other revenues" jumped significantly this past quarter by an impressive 53% from last year's 1.05 billion to 1.6 billion. This segment includes app download revenue, including a large array of games, which is an area of focus for Google. Figure 1 shows how Google has been able to successfully increase revenue since the first quarter of 2008.(click to enlarge) While there were many strong points reported within this earnings report, Google's declining cost-per-click (CPC) for Google's sites were down 7% and average CPC declined 6% since last year. Pricing pressure has increased and will continue to increase due to Facebook's strong mobile ad growth.

I Know First-Daily Market Forecast, does not provide personal investment or financial advice to individuals, or act as personal financial, legal, or institutional investment advisors, or individually advocate the purchase or sale of any security or investment or the use of any particular financial strategy. All investing, stock forecasts and investment strategies include the risk of loss for some or even all of your capital. Before pursuing any financial strategies discussed on this website, you should always consult with a licensed financial advisor.