The article was written by Motek Moyen ResearchSeeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

Summary:

I made a buy recommendation for AAPL last November when it was trading below $265. I gave it a 90-day price target of $290.

Apple’s stock set a new record price of $312.67 and closed at $310.33 last January 10, 2020.

You can do profit taking now or add more Apple shares. My bet is that AAPL can still soar higher. My new 90-day target is $325.

Apple is still the most profitable smartphone company. Android phone vendors are hurting themselves with their pricing war.

Even though its notably more expensive than other flagship 2019-era Chinese Android phones, the older iPhone XR is still the world’s best-selling smartphone.

This article was written by the I Know First Research Team.

The infamous Apple logo

Apple (NASDAQ:AAPL) has come a long way over the past few years. As it has doubled its stock price since summer 2016 and become the first trillion dollar company earlier this year, it has also seen some dips and is currently below the price it was at a year ago.

Apple is now down 33% from it’s all time high of 233.47 and has dropped below the trillion dollar mark once again. Apple’s most recent tumble has left the company at a new 2018 low ~$150 on December 21 causing market cap to drop below $700 billion for the first time in nearly 2 years. So what’s next for the company for the next year? Will the stock price continue to slump as it has for the tail end of 2018? Or will it bounce back for another record breaking year? In this article, we will take a look at Apple’s strengths, weaknesses, opportunities, and threats in order to determine the tech giant’s future potential.

SWOT Analysis

Strengths

Apple has many strengths that have helped it stay on top of the phone and computer market for years. It’s simple and easy to use iOS phone software compatibility with its macOS computer software has allowed consumers to maintain seamless connections between their phones and computers. This has contributed to the large brand loyalty customers feels towards Apple. Many iPhone users have used the flagship phone for years and do not plan on switching anytime soon.

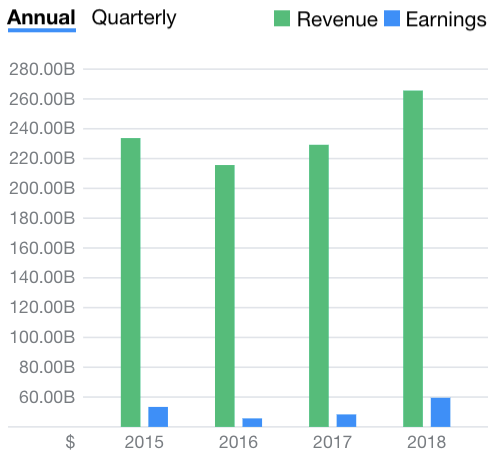

Moreover, Apple has boasted strong financials over the past years with strong quarterly reports. While some investors were not necessarily thrilled with the company’s latest Q4 earnings report, there were still many impressive metrics such as a 20% YoY increase in revenue to $62.9 billion. This translated to an extraordinary 41% YoY increase in earnings per share of $2.91. These high percentages resonate more with those of a startup than the multibillion dollar company Apple has become.

Source: Yahoo Finance

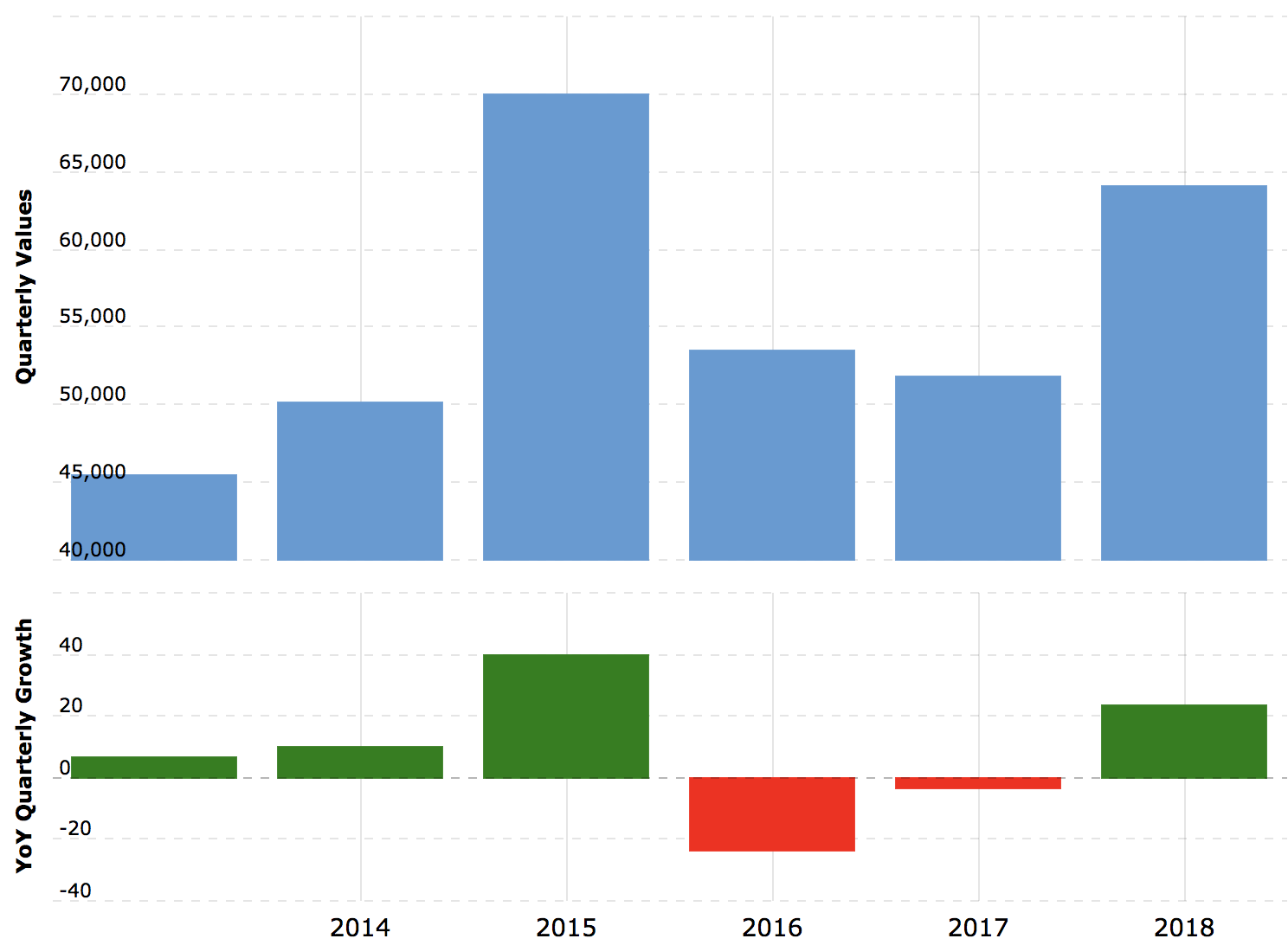

These high revenues have given the company high cash flow it can invest as it chooses. The company has put a large focus on research and development of its current products as well as new ventures. For example, the company releases new iterations of its phones, computers, and watches yearly. On top of that, the company has been working on new applications of its technology such as self-driving cars. In the past, Apple has created innovative products that have helped attract and maintain customers.

Apple Annual Free Cash Flow (Source: MacroTrends)

Despite being a multibillion dollar company, Apple still have a relatively fair valuation. The company’s Price/Earnings Ratio is cheaper than the industry average which sits around 20. This is also very valid considering it also has a very reasonable forward P/E of 11.85. Additionally, Apple’s earnings growth doesn’t seem to be stopping. Over the past 5 years, EPS growth has been around 15%. Over the next 2 years, EPS is expected to grow by a slightly lower, but still significant 11.10%.

Weaknesses

While Apple did have a strong start to the year, it struggled in the final quarter of the year. Despite announcing three new iPhone models in September, the company did not meet expectations for unit sales. While this would have been disheartening, but not necessarily worrisome on its own, Apple also announced it would no longer release metrics for hardware unit sales. To many investors, this implied a slowdown of sales and potentially a dip into negatives.

One of the most unique features of the iPhone XR is the new color ways available. Although some of these colors were also available for Apple’s last budget phone, the iPhone 5C (Source: Apple)

So why exactly have iPhone sales been down? With improvements in the technology within smartphones, they now last longer and consumers do not necessarily need one every year or two. Additionally, the latest iteration of iPhones were extremely similar to the previous generation, leading few people with newer phones to upgrade. In the past, the new features of the most recent iPhone might still incentivize those with functioning phones to take the plunge for the news phone, now only those who are in need of new phone will invest. Additionally, the high price of the iPhone XS and iPhone XS Max may be a pinnacle for Apple’s pricing power. Even the company’s cheaper option, the iPhone XR, sells for a premium of $749. The higher prices for fewer new features has led consumers to use their phones for longer and hold off on upgrading, decreasing hardware sales.

On January 2, Apple released a press release outlining a revised lower guidance for the upcoming quarter. This sent the Apple stock tumbling as investors began worrying about these lower earnings. Apple cited four primary reasons for the decreased expectations: launch timing, foreign exchange conversions, supply constraints, and difficulty in emerging markets. The most significant weakness to Apple is the lack of revenue from iPhones which the company attributes to the timing of its launch. Because of the delay in the iPhone X, many of the orders were fulfilled in Q1 2018 whereas the majority of iPhone sales were fulfilled in Q4 2018 for the iPhone XS, iPhone XS Max, and iPhone XR. This in combination with supply constraints urged Apple to warn its investors of lower potential revenue for the first quarter of 2019.

Opportunities

While iPhones still represent Apple’s core business, Apple has been diversifying its revenue by focusing on its services. While buying an iPhone or other Apple hardware product happens at most once a year, services can be purchased at anytime with higher frequency. Apple’s Services division is composed of many different services ranging from AppleCare, Apple Pay, Apple Music, and more. In its most recent quarter, Services revenue increased 17% YoY to nearly $10 billion. If Apple continues to focus on the Services market, it can reap large profits.

Apple also recently teamed up with Amazon to form a lucrative new partnership. Amazon will now be a direct reseller of Apple iPhones and iPads. This should help to boost hardware sales and sets the stage for future partnerships with Amazon which should prove profitable for Apple. This partnership also allows Apple the chance to capitalize on another opportunity: holiday sales. The holiday season has high potential to increase hardware sales.

Another potential, but less likely partnership may be with Tesla. Many analysts have noted that the companies similar emphasis on seamless software and sleek hardware could lead to either an acquisition or partnership. While there has been no indication from either company that this is in the works, it would be logical considering Apple’s work on self driving cars and Tesla’s need for free cash flow.

Apple has struggled in the past with developing markets such as in India. The expensive iPhone has not had the massive success it has in other countries because of many lower price alternatives from competitors. Additionally, high tariffs have made the phones come at an even higher premium. Apple began combatting this by starting to assemble iPhones such as the SE and 6S in 2017 through Wistron’s local unit in Bengaluru. Apple has now struck a deal with Foxconn to being manufacturing its newer iPhones such as the iPhone X in the beginning of 2019. Until now the company has only sold is lower end models, so the introduction of new premium phones will hopefully grow Apple’s prominence in the country. This partnership has massive potential to help Apple gain market share in the huge Indian phone market.

Threats

Source: Pixabay

In December, the US market officially entered bear territory, just like Apple itself. Many stocks are struggling in December, one of the usually most profitable months for companies. As one of the biggest stocks in the US stock market, Apple can be affected by general market sentiment and trends like this December dip. With many analysts wary of an oncoming recession, Apple could suffer from no fault of its own.

Another potential threat Apple faces is an escalating US-China trade war. Just like the entire technology sector, Apple is susceptible to impacts from tariffs. Additionally, Apple faces pressure to move production to US which would lead to higher costs for Apple. Meanwhile, China has proposed various policies from closing its markets which would affect many Apple suppliers. On top of this, Apple is currently appealing an iPhone sales ban in China and Germany on older iPhone models over patent infringements of Qualcomm. A Chinese court has banned imports and sales of iPhones comprising approximately 10-15% of Apple’s China sales. However, Apple will continue selling its iPhone 7 and 8 models on the website while the decision is appealed.

The trade war is not the only difficulty Apple is facing in regards to international expansion. Another major player in Apple’s lower revenue guidance was difficulty in emerging markets and significantly lower iPhone sales in China. As a whole, China’s economy has been slowing down since the middle of 2018. This economic slowdown was only exacerbated by trade tensions leading to a large contraction in the smartphone market that affected Apple and created a revenue shortfall. Apple also overestimated the number of upgrades in these emerging markets which is a result of a strong US dollar, fewer subsidies, and phones now function at a high capacity for much longer than they used to. Apple is already taking action to minimize the impact of these threats in the future.

Analyst Recommendations

Currently, the majority of analysts have a bullish outlook for AAPL. Of the 42 analysts polled by Yahoo Finance, 31 rate Apple stock as a Buy with 11 of these as Strong Buy. Only 11 of the analysts give Apple a neutral rating.

Conclusion

Despite lowered earnings expectations, which has been a very bearish signal for many investors, Apple still has potential in the new year. While Apple cannot control the macroeconomic environment that has led to this decreased guidance, the company is already combating these with new programs. For example, Apple is now incentivizing customers to upgrade their iPhone by offering larger trade in values for older models. Additionally, which iPhone sales have suffered, the largest number of iPhones are being used daily which provides a large market for Apple’s services and also exemplifies the loyalty of Apple users. The price drop that resulted from Apple’s press release now provides an even more valuable opportunity to buy into the multibillion dollar company.

While Apple does have some weaknesses to work on and threats to combat, the company has many strengths and opportunities it is building on while should outweigh the downside. That being said, as the economy sinks into bearish territory and trade war tensions continue building, the market as a whole including Apple, will probably not see any major gains. Over the long run though, Apple should bounce back. As it diversifies its revenue by taking advantage of Apple Services, the offset of decreased hardware sales will affect earnings less. Additionally, with a track record of new innovation, Apple’s next line of phones should be more unique. Moreover, no one knows what other products are in development. Based on this, Apple should be back in winning territory by the end of 2019.

The article was written by Motek Moyen ResearchSeeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

Summary:

This holiday quarter should see a notable increase in Apple’s hardware sales. Apple’s flat lining iPhone unit sales desperately needs a boost.

Amazon recently agreed to sell Apple Watches, iPhones, and iPad tablets in its U.S. and international online stores.

Amazon agreed to become an official Apple reseller. Amazon will delist unauthorized resellers of Apple products using its platform by January 4, 2019.

Amazon touts more than 100 million Prime subscribers. They are all desirable potential customers for Apple products. Buying online is faster than queuing up at an Apple retail store.

“Innovation distinguishes between a leader and a follower.”

-Steve Jobs

Summary

Apple announced strong Q4 results, nevertheless the stock declines Outlook on Future Sales and Profits look promising Apple is launching a new streaming service and are facing high competition Risky investment environment around the world

The article was written by Hieu Nguyen, a Financial Analyst at I Know First.

“Here’s a company with, whatever their earnings are, $60 billion, and you can put all their products on a dining room table. Nobody buys a farm based on whether it’s going to rain next year, they think it’s a good investment over 10 or 20 years.” “– Warren Buffett

Summary:

Apple Q2 2018 Results: Tim Cook one more time proved that he was right

Where is the future of iPhone?

Three different valuation methods all agree at a long-term Buy recommendation for Apple

(Source: Wikimedia Commons)

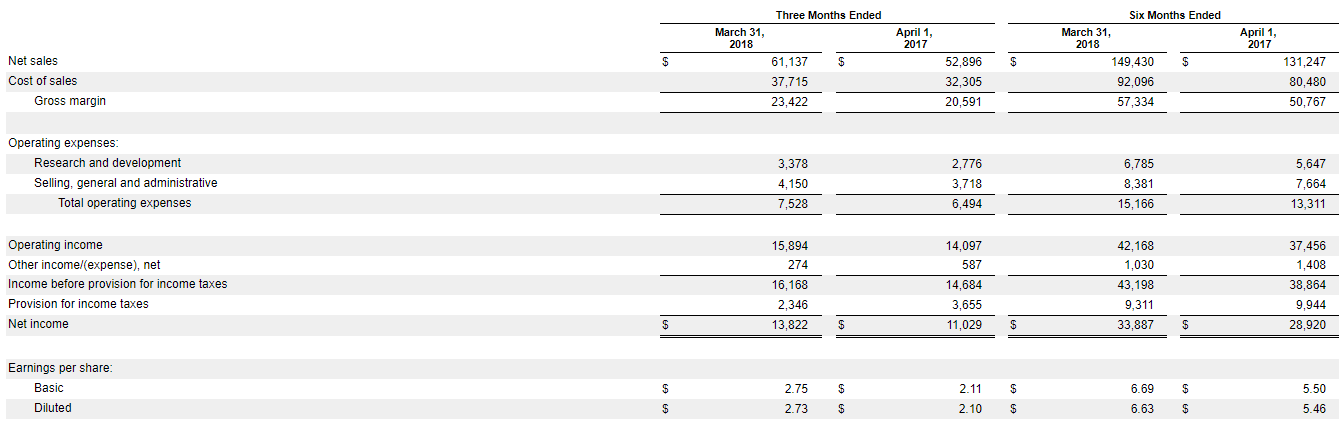

Q2 2018 Results: Tim Cook one more time proved that he was right.

On May 2nd, Apple Inc. (NYSE: AAPL) released its quarterly report. Apple’s net sales have grown 15.58% quarter over quarter, and 13.85% compared to the last 6 months. Although the gross profit margin dropped by 61 basis points, net income and EPS jumped up by 25.32% and 28.44%, respectively. A major contribution for the strong growth is iPhone sales. Despite of the fact that Wall Street considered iPhone X to be pricey, its performance is still very impressive. iPhone unit sales slightly increased by 3% but thanks to the increase in price, the total sales increased by 14%.

On the other hand, Mac witnessed a stable revenue from Q1 2017. The premium laptop from Apple has been facing with competions from other premium brands such as HP Spectre, Lenovo ThinkPad, or Dell XPS. Furthermore, earlier this month, Apple admitted its faulty MacBook keyboard. In 2015, Apple launched a new keyboard that Apple claimed to be 40% thinner. However, customers began to report problems with this type of keyboard, forcing Apple to fix the keyboard, free of charge.

About services, Apple reported a 31% growth rate in this segment. Thanks to the deferrals and amortization of the software, Apple services revenue is expected to continue to increase at a double-digit growth rate. According to Fortune, over the first quarter, Apple shipped 600 thousand HomePod along with 8 million Apple Watch. Despite a strong growth of more than 55%, both sales and unit sales of Apple Watch are far below the three main products: iPhone, iPad, and MacBook.

Where is the future of iPhone?

It has been more than 7 years from the day that Steve Jobs left Apple. In fact, with remarkable successes of the first four iPhone generations, Steve Jobs has set a very high bar for his successor, Tim Cook. Since then, every time Apple released their new iPhone, users have not been surprised the way they had been in the first 4 iPhones. As we can see from the table under, there were not many developments since iPhone 6S. The most significant improvement is the Face ID technology in iPhone X.

However, both of the sales and number of unit sold have continued to grow year over year. Since 2012, after Steve Job left Apple, it has grown 13.8% in sales and 10.8% in unit sold. Since it was release, iPhone X has been considered to be too pricey and Wall Street expected the slow down of the revenue. It turned out that iPhone revenue still grew at 14% in the first two quarters. Moreover, customers are still very happy about their premium smart phone. According to Luca Maestri, Apple’s senior vice president and CFO: “The latest survey of U.S. consumers from 451 Research indicates that across all iPhone models, the customer satisfaction rating was 95%, and combining iPhone 8, 8 Plus and iPhone X, customer satisfaction was even higher, at 99%.”

On the other hand, Apple has been facing a tremendous competition. Undoubtedly, Apple in general and iPhone in particular has been a technology symbol all over the world. Although they are still one of the market leaders, the expansion of other brands especially in Chinese market are considerable. Since iPhone is the strongest brand of Apple, the company needs to renovate its product if it does not want to be surpassed by the competitors.

The War of Artificial Intelligence: Siri is far behind Google Assistant, Alexa, and even Cortana

Apple HomePod’s market share is far below Amazon Echo and Google Home. According to Fortune, HomePod only has 3% of the market share while this number of Amazon Echo and Google Home are 55% and 23%, respectively. Apple is also struggling with HomePod marketing. When Amazon Echo is considered an online shopping assistant and Google Home can answer almost all of your questions, Apple tries to market HomePod as a music reinvention. However, so far, Apple has not succeeded with this strategy.

Moreover, Siri is considered not as smart as the its competitors. Based on a research from Stone Temple, while being asked 5000 questions, Google Assistant tried to answer 75%, Cortana tried two third, Amazon Alexa tried about a half, while Siri could only try 40%. Besides that, in May 2018, to dominate the AI assistant industry, Microsoft Cortana has co-operated with Amazon Alexa. While Cortana can help users during their working time, Alexa will assist them during their free time. In another move, Google also showed how their AI assistant can make a real phone call. As a result, if Apple’s engineers will do nothing, Siri will be out of the AI game sooner or later.

(Source: Wikimedia Commons)

3 methods of Valuation all agree That Apple Stock Is Undervalued

DCF Valuation

Our 5-year DCF analysis arrives the target price of $207.95 for AAPL. DCF model was constructed based on 3 main factors: top line and bottom line forecast, capital expeditures, and WACC. Two third of Apple’s revenue comes from iPhone. However, as we analyzed above, the company is facing with a lot of difficulties to increase the unit sold. On the other hand, the price of iPhone X and iPhone 8 has already been high compared to the premium smart phones on market. Hence, we do not expect the sales to grow faster in the future. Morover, CAPEX is expected to grow at around 10% in the next five years.

The most three important factor that will impact the value of the company is iPhone sales, gross profit margin, and CAPEX. I ran a Monte Carlo Simulation with these three variables to see how the stock price will response to each variable. More than 73.18% of the result are within the Hold recommendation (within 10% of the current price) while 26.66% is a Buy recommendation

Dividend Discount Model

The second method to be used is Dividend Discount Model. Based on the 5 years historical data, Apple has used about 88%-94% of its net income to pay dividend and stock repurchase. As a result, we used two-stage discount model to calculate the value of AAPL. We assume that the company will not repurchase stock in the future but pay out dividend at the payout ratio of 91% net income. With the discount rate of 9%, the target price based on this method is $220.40, 19.18% upside. This method agrees with the previous method in a Buy recommendation in the stock.

Multiple methods

In fact, Apple is a unique company within its industry. Hence, it is no such a good peers that we can use for multiple method. However, we can compare Apple with the other big four technology giants include Alphabet, Amazon, Facebook, and Microsoft. As we can see, all of the P/E, P/B, and EV/EBITDA of Apple are lower than than the average of the other big four. We can not tell that just because the ratios are lower, the stock is expected to grow. However, Wall Street seems to undervalue Apple among the other technology giants.

Conclusion

Apple still one of the market leaders in both smartphone and laptop industry. Unlike Wall Street expectation, Apple’s Q2 2018 results showed strong growth in both sales and net income. The main contribution is from iPhone. However, all of the Apple products are facing with a lot of competitions, requiring the company to renovate. Using three different valuation methods, we agree on a BUY recommendation for the stock.

Current I Know First Algorithm Bullish Forecast for AAPL:

My recommendation is supported by the I Know First algorithm bullish forecast for AAPL. On June 25th, 2018, I Know First issued a forecast for AAPL with a strong 1-year bullish signal of 150.20 and a very high predictability of 0.81. In addition, the signal gets better over the time. The prediction totally agrees with the above arguments about the future of Apple.

“If you’re going to make connections which are innovative… you have to not have the same bag of experiences as everyone else does.” – Steve Jobs

Highlights:

Apple on the way to a breakthrough – carbon-free aluminum smelting

Financial Results for fiscal Q2 of 2018

Q3 Financial Guidance

Industrial comparison

[Image Source: Fossbytes.com]

Apple on the way to a breakthrough – carbon-free aluminum smelting method

Aluminum is a key material in many of Apple’s most popular products, and for more than 130 years, it’s been produced the same way. Aluminum giants Alcoa Corporation and Rio Tinto Aluminum announced a joint project to commercialize original technology that eliminates direct greenhouse gas emissions from the traditional smelting process. This is a key step in aluminum production that if fully developed and implemented, will strengthen the closely integrated Canada-United States aluminum and manufacturing industries.

As part of Apple’s commitment to reducing the environmental impact of its products through innovation, the company helped accelerate the development of this technology. Apple has partnered with both aluminum companies, and the Governments of Canada and Quebec, to collectively invest a combined $144 million to future R&D. “Apple is committed to advancing technologies that are good for the planet and help protect it for generations to come,” said Tim Cook, Apple’s CEO.

This follows Apple’s announcement last month that all of its facilities are now powered with 100 percent clean energy and 23 of its suppliers have committed to do the same.

[Image Source: GlobalMediaIT]

Q2 Financial Results of 2018

On May 1st, 2018, Apple announces its financial Q2 results of 2018. Apple achieved a quarterly revenue of $61.1 billion, 16% increase from Q2 of 2017, quarterly earnings per diluted share of $2.73, up 30%, and generated over $15 billion in operating cash flow. International sales accounted for 65% of the quarter’s revenue. In Q2, iPhone X was sold more than any other iPhone each week and the company’s revenue in all geographic segments grew, with over 20% growth in Greater China and Japan. As for this financial Q2 report, Apple’s board has approved a new $100 billion share repurchase authorization and a 16% increase in their quarterly dividend. Reflecting the approved increase, the board has also declared a cash dividend of $0.73 per share of Apple’s common stock.

Apple is expected to continue to net-share-settle vesting restricted stock units. From the inception of its capital return program in August 2012 through March 2018, Apple has returned $275 billion to shareholders, including $200 billion in share repurchases.

The Company will complete the execution of the previous $210 billion share repurchase authorization during Q3.

Q3 of 2018 Financial Guidance

Revenue between $51.5 billion and $53.5 billion Gross Margin between 38% and 38.5%

I Know First-Daily Market Forecast, does not provide personal investment or financial advice to individuals, or act as personal financial, legal, or institutional investment advisors, or individually advocate the purchase or sale of any security or investment or the use of any particular financial strategy. All investing, stock forecasts and investment strategies include the risk of loss for some or even all of your capital. Before pursuing any financial strategies discussed on this website, you should always consult with a licensed financial advisor.